Rent explained

Rent is the periodic payment to an entity for the use of their property. Rent is paid by individuals and organizations for the use of a variety of types of property, equipment, vehicles, or other assets.

In this article, we will cover five types of rent payments: base rent, prepaid rent, accrued rent, deferred rent, and variable rent (also known as contingent rent).

Accounting for rent under the new lease accounting standards

Recent updates to lease accounting, including new standards ASC 842, IFRS 16, GASB 87, SFFAS 54, and FRS 102 have changed the accounting treatment for some types of leasing arrangements. In short, organizations will now have to record both an asset and a liability for their operating leases. Under the old lease accounting rules, the cash payments for operating leases were recorded as rent expense in the period incurred and no impact to the balance sheet was recognized.

Under ASC 842, the new lease accounting standard effective for all US GAAP entities beginning in 2022, organizations record a lease liability equal to the present value of the remaining lease payments and a right-of-use (ROU) asset equal to the lease liability plus a few adjustments (if applicable). Lease payments decrease the lease liability and accrued interest of the lease liability. A lease expense, equivalent to the straight-line rent expense recognized under ASC 840 for operating leases, is recognized for interest accrued on the lease liability and amortization of the ROU asset.

The periodic lease expense for an operating lease under ASC 842 is the product of the total cash payments due for a lease contract divided by the total number of periods in the lease term. If all details of a contract are the same, organizations record the same amount for lease expense under ASC 842 as they would for rent expense under ASC 840.

Both rent expense and lease expense represent the periodic payment made for the use of the underlying asset. To that end, these words are often used interchangeably. Organizations may have a commercial leasing arrangement or a rental agreement. However, since lease expense is a relatively new term to accounting when compared to rent expense, other terminology such as base rent, variable rent, prepaid rent, and deferred rent are referred to primarily as rent and have not yet switched to lease-related terms.

Keep in mind however, rent or lease expenses are related to operating leases only. If an entity has a capital lease (now known as a finance lease under ASC 842), payments reduce the capital lease liability and accrued interest, and are therefore not recorded to rent or lease expense. In some instances, agreements to pay an entity for the use of their asset may not fall within the scope of ASC 840 or ASC 842, but payments for these contracts may still be recorded as lease or rent expense on the lessee’s income statement.

Base rent

Base rent, also known as fixed rent, is the portion of the rent payment explicitly stated in the contract. A leasing contract may include a payment schedule of the expected annual or monthly payments. Even if the contract includes escalation increments to the beginning or base payment amount, this type of rent is fixed. It is presented in the contract, along with planned increases, and will not change over the contract term without an amendment.

When the periodic payments are structured so they can not be calculated without the occurrence of an event, such as a number of sales or units produced, the payments are not considered fixed rent.

Accounting for base rent with journal entries

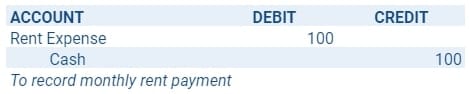

Under ASC 840, accounting for and recording base rent was very simple. No liability or asset was required to be established for an operating lease. The lessee would have recorded a debit to rent expense and a credit to cash to represent the expense for the usage of the asset incurred during the period and payment for that expense in the same period:

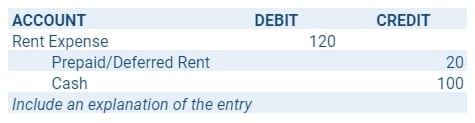

If the contract was significant and rent varied over the lease term, the correct accounting treatment was to add all of the rent payments over the lease term and divide by the total number of periods to calculate the straight-line rent expense. Straight-line rent expense results in recognizing the same amount of rent expense in each period during the lease term regardless of the payment amount for the period. Therefore, the entry to record straight-line rent was a credit to cash for the rent payment specified in the contract, a debit to rent expense for the calculated straight-line amount, and a debit/credit for the difference between the two to prepaid/deferred rent:

Under ASC 842 base rent is included in the establishment of the lease liability and ROU asset. The amortization of the lease liability and the depreciation of the ROU asset are combined to make up the straight-line lease expense. Similarly to ASC 840, this straight-line lease expense is calculated as the sum of all of the rent payments over the lease term and divided by the total number of periods. A full example with journal entries of accounting for an operating lease under ASC 842 can be found here.

Download our Ultimate Lease Accounting Guide for more examples:

Prepaid rent

Prepaid rent is a lease payment made for a future period. A company makes a cash payment, but the rent expense has not yet been incurred so the company has prepaid rent to record. Prepaid rent is an asset – the prepaid amount can be used by the entity in the future to reduce rent expense when incurred in the future.

The primary indicator for prepaid rent is timing. The tenant is paying for an expense that has not yet been incurred. Consistent with the matching principle of accounting, when the rent period does occur, the tenant will relieve the asset and record the expense. A typical scenario with prepaid rent is mailing the rent check early so the landlord receives it by the due date.

For example, an organization’s building rent is due by the first of the month. For the check to reach the landlord and post by the first, the organization writes the check the week before on the 25th. When the check is written on the 25th, the period for which it is paying has not occurred. Therefore the check is recorded to a prepaid rent account for the timeframe of the 25th through the end of the month. On the first day of the next month, the period the rent check was intended for, the prepaid rent asset is reclassed to rent expense.

Is prepaid rent an asset?

Under ASC 840, prepaid rent was recorded as an asset. However, under ASC 842, the new lease accounting standard, prepaid rent is now included in the measurement of the ROU asset. Any prepaid rent outstanding as of the transition is included in the measurement of the ROU asset. Subsequent lease accounting under ASC 842 also requires any prepaid amounts to be recorded to the ROU asset.

Accounting for prepaid rent with journal entries

When rent is paid in advance of its due date, prepaid rent is recorded at the time of payment as a credit to cash/accounts payable and a debit to prepaid rent. When the future rent period occurs, the prepaid is relieved to rent expense with a credit to prepaid rent and a debit to rent expense.

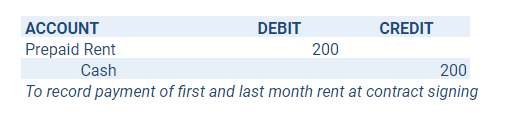

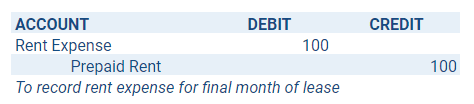

Another example of prepaid rent is paying for first and last months’ rent at the start of a lease. The initial payment for first and last months’ rent is made at the signing of the lease agreement prior to the lease commencement date. The journal entries for prepaid rent under ASC 840 are shown below:

At the beginning of the first month the tenant occupies the property and owes rent, the tenant would incur one month of rent expense and relieve the prepaid rent with the following entry:

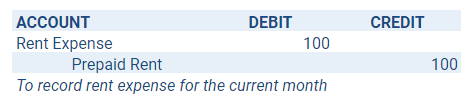

The tenant keeps one month of prepaid rent on the books until the last month of the lease agreement at which time this entry is recorded:

Under ASC 842, you would see the same entries, but the prepaid rent would be recorded to the ROU asset in place of a separate prepaid rent account. Additionally, at the time of transition to ASC 842, any outstanding prepaid rent amounts would be included in the calculation of the appropriate ROU asset.

Note: To learn more about accounting for other prepaid expenses, read “Prepaid Expenses Guide: Accounting, Examples, Journal Entries, and More Explained.”

Accrued rent

In contrast to prepaid rent is the rent liability – accrued rent. Accruals represent an obligation for an expense incurred but not paid. In the case of a rent accrual, the company records the rent expense but the payment is not yet due. An example of this is rent which is paid quarterly.

Accounting for accrued rent with journal entries

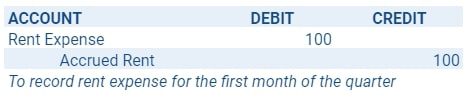

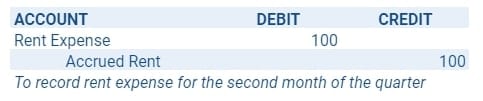

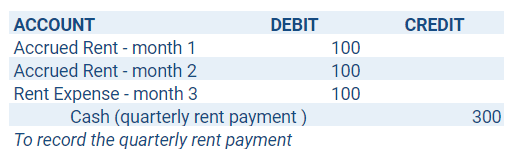

Let’s assume rent is due at the end of the quarter. The expense for the first two months has been incurred because the company has used the rented equipment or occupied the leased space, but cash for these services has not been paid. The company has recorded rent expense for the first two months of the quarter but they have an accrual for the payment. When payment is sent for the last month of the quarter, the company will record the current month’s rent expense and debit the accrual for the two months not yet been paid, all offset by the cash payment – a credit for all three months’ rent expense.

The entries under ASC 840 looked like this:

At the end of the second month, the company has two months of rent payments accrued with two months of rent expense recognized. The entry when the quarterly rent payment is made in the last month of the quarter is as follows:

Similar to the treatment of prepaid rent, under ASC 842 the accruals are recorded to the ROU asset instead of a separate accrued rent account.

Deferred rent

Deferred rent is a liability account representing the difference between the cash paid for rent expense in a given period and the straight-line rent expense recognized for operating leases under ASC 840. When a rent agreement offers a period of free rent, payments are not due to the lessor or landlord. However, you are recording the straight-line rent expense calculated by dividing the total amount of required rent payments by the number of periods in the lease term. Additionally, deferred rent is also recorded for lease agreements with escalating or de-escalating payment schedules.

Accounting for deferred rent with journal entries

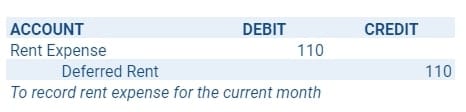

During the months no rent payments are due, the entry recorded is:

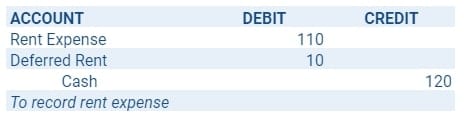

In a scenario with escalating lease payments, the average expense recorded is more than the lower payments at the beginning of the lease term. A balance accumulates in the deferred rent account. Eventually, the lease payments increase to be greater than the straight-line rent expense. In the case of the rent abatement above, the company begins paying rent but the payments are larger than the average rent expense which includes the abatement period.

Accordingly, subsequent entries for both scenarios look like this:

By the end of the lease, the balance in the deferred rent account will be zero.

Deferred rent is primarily linked to accounting for operating leases under ASC 840. Nevertheless, differences between lease expense and lease payments also exist under ASC 842. In contrast, under the new accounting standard, both the accumulation and reduction of a deferred rent balance are being recognized in the financial statements as part of the ROU asset rather than in a deferred rent account. This comparison of deferred rent treatment under ASC 840 and ASC 842 is illustrated in Deferred Rent Accounting and Tax Impact under ASC 842 and 840 Explained.

Variable/contingent rent

In comparison to the description above, variable rent, sometimes called contingent rent, is rent based on an event that has not yet occurred. Some examples of variable rent include but are not limited to:

- Rent based on a specific performance, such as a percentage of sales or revenue

- Rent based on usage, such as miles driven or units produced

- Rent based on the occurrence of an event

Accounting for variable/contingent rent

Generally, variable, or contingent rent, is expensed as incurred according to both legacy accounting and the new accounting standard. When the rent agreement specifies rent is based upon a performance or usage, the rent amount will not be included in the measurement of the lease liability because the amount of performance or usage is not known at the commencement date. Therefore, no amount is available on which to base the rent calculation. This treatment is the same under ASC 840 and ASC 842.

If the lease agreement defines the rent payments as contingent upon a performance or usage but also includes a minimum threshold, the minimum is used in the calculation of the lease liability. Because of the inclusion of the minimum threshold, the lessee has a commitment to pay at least the lower amount regardless of actual performance or usage. These types of payment terms are known as in-substance fixed rent. While some variability exists in the outcome of the calculation, the minimum amount is fixed.

Similar to fixed rents, the minimum rent is also included in the straight-line rent calculation for operating leases under ASC 840 and the calculation of the lease liability under ASC 842. When the actual rent amount is paid, any variance from the minimum threshold used in the initial valuation is recorded directly to rent or lease expense.

If the lease payment is variable the lessee cannot estimate a probable payment amount until the payment is unavoidable. Even if a high certainty the performance or usage the variable lease payment is based on will be achieved does exist, the payments are not included in the lease liability measurement. While it is highly probable performance or usage will occur, neither of these things are unavoidable by the lessee until after they have been completed.

An example of accounting for variable/contingent rent

For both the legacy and new lease accounting standards, the timing of the rent payment being known is the triggering event. For example, let’s examine a lease agreement that includes a variable rent portion of a percentage of sales over an annual minimum. At the initial measurement and recognition of the lease, the company is unsure if or when the minimum threshold will be exceeded. Therefore the variable portion of the rent payment is not included in the initial calculations, only expensed in the period paid.

Download our Ultimate Lease Accounting Guide for more examples:

Summary

To summarize, rent is paid to a third party for the right to use their owned asset. Renting and leasing agreements have existed for a long time and will continue to exist for individuals and businesses. With the transition to ASC 842 under US GAAP, some of the terminology and accounting treatments related to rent expense are changing.

On the other hand, the impact to the income statement and balance sheet regarding the accounting treatment of rent expense is unsubstantial, specifically regarding fixed rent, variable rent, prepaid rent, accrued rent, and deferred rent. In conclusion, accounting for rent expense is changing insignificantly from ASC 840 to ASC 842. Now if only the same thing could be said about the accounting for operating leases.