1. What is accrual accounting?

2. Key components of accrual accounting

3. Cash basis vs. accrual basis accounting

4. Benefits of accrual accounting

5. Challenges of accrual accounting

6. When should you use accrual accounting?

7. Industry specific applications of accrual accounting

8. Example: Accrual accounting for prepaids

9. Example: Accrual accounting for accruals

10. Summary

11. Frequently asked questions

12. Related articles

In this article, we will explore the fundamentals of accrual accounting, dive into its key components including prepaids and accruals, compare it with cash basis accounting, and provide real world examples to illustrate its application. We will also look at various applications and industry-specific considerations to help you understand how this accounting method plays out in practice.

What is accrual accounting?

Accrual accounting is a method of accounting where revenues and expenses are recorded when they are earned or incurred, rather than when cash is received or paid. This method is designed to match income with the expenses that were incurred to generate that income, which results in a clearer view of a company’s financial position.

Under the accrual basis of accounting:

- Revenues are recognized when they are earned.

- Expenses are recognized when they are incurred.

This method aligns with the matching principle, a fundamental concept in accounting that dictates expenses should be matched with the revenues they help to generate in the same accounting period.

This approach also supports the revenue recognition principle, which ensures that revenue is recorded in the same period it is earned, even if the payment is delayed. These principles together contribute to a more consistent and comparable financial statement presentation across periods and among different companies.

Accrual accounting provides the framework for recording complex transactions such as credit sales, deferred revenues, long-term service contracts, and employee benefits, which are not immediately settled with cash.

We will now look at some of the key components that make up accrual accounting.

Key components of accrual accounting

Prepaid expenses

Prepaid expenses are payments made in advance for goods or services that will be received in the future. These are initially recorded as assets on the balance sheet and gradually expensed over the periods to which they relate.

Example of a prepaid expense: Imagine a company pays $12,000 on January 1st for a one-year software agreement. Under accrual accounting, the company does not recognize the full $12,000 as an expense in January. Instead, it records a $12,000 prepaid software asset, and each month, it recognizes $1,000 ($12,000 ÷ 12 months) as a software expense. This continues until the end of December when the prepaid account is fully expensed.

Other common examples of prepaid expenses include rent, insurance, software subscriptions, and maintenance contracts. These expenses are considered current assets and are expected to benefit the company within the current year.

Accruals

Accruals refer to revenues earned or expenses incurred which have not yet been recorded through a cash transaction. These are necessary to ensure the financial statements reflect the economic activity of a company accurately for the specific reporting period.

Example of an accrual: Suppose an employee earns $5,000 in the last week of December, but the company does not pay this amount until the first week of January. Under accrual accounting, the company would record a salary expense and an accrued liability of $5,000 in December, even though the payment occurs in the following month. This ensures the expense is recognized in the period it was incurred.

Additional examples of accruals include utilities used but not yet billed, accrued interest on loans or investments, and income from services performed that will be billed in a subsequent period.

Deferrals

You may have also heard of deferrals when looking into the accrual method of accounting. The term, “deferral,” can refer to either a deferred expense or deferred revenue. For example, within the Conceptual Framework, FASB lists prepaid expenses and customer deposits as two common types of deferrals.

“Deferred expense” is another term for a prepaid expense and these terms are often used interchangeably.

Deferred revenue is an instance where payment is received but the service or goods have not yet been delivered resulting in deferred revenue recognition. A simplified version of FASB’s definition of deferrals is, “The accounting process of recognizing a liability resulting from a current cash receipt with deferred recognition of related revenues, expenses, gains, or losses.” Deferred revenues are often associated with ASC 606 and can have tax implications.

To learn more about the differences between accruals and deferrals, read our blog, “Accrual vs. Deferral Explained: Back to Basics.”

![]()

Cash basis vs. accrual basis accounting

Understanding the difference between cash basis and accrual basis accounting is crucial for business owners and accounting professionals. We’ll explore the key differences between the two methods as well as the advantages and disadvantages of both methods.

Cash basis accounting

Cash basis accounting recognizes revenues and expenses only when cash is exchanged. It is simpler and more straightforward, often used by small businesses and sole proprietors.

Advantages:

- Simplicity.

- Better cash flow tracking.

- Fewer adjusting journal entries needed.

Disadvantages:

- Does not match income with related expenses.

- May not accurately reflect the company’s current financial position.

- Not compliant with GAAP or IFRS for most entities.

Accrual basis accounting

Accrual basis accounting, as discussed, records financial events when they occur, regardless of cash flow. This often will result in a more accurate representation of a company’s financials for a given period.

Advantages:

- Provides a more accurate financial picture.

- Complies with GAAP and IFRS.

- Better suited for performance measurement.

Disadvantages:

- More complex to maintain.

- Requires more robust accounting systems.

- More difficult to track cash flows.

Example to compare: Let’s say a company delivers a service in December worth $20,000 but receives payment in January.

- Under cash basis accounting, the revenue is recorded in January.

- Under accrual accounting, the revenue is recorded in December, when the service was performed.

This difference can either positively or negatively influence the financial statements which can then skew the outlook for financial statement users.

Benefits of accrual accounting

Accrual accounting offers several advantages that make it the preferred method for most businesses:

- Greater financial insight: By recognizing transactions when they occur, businesses gain a better understanding of their actual financial performance.

- Better decision making: Accurate financial reports allow management to make informed decisions.

- Regulatory compliance: Most accounting frameworks and regulatory bodies require accrual accounting for external reporting.

- Consistency in reporting: Accrual accounting helps keep consistent reporting periods, which is key for tracking performance trends.

- Financial statement users confidence: Financial statement users prefer accrual-based reports because they present a more realistic picture of a company’s financials.

- Better credit terms: Businesses using accrual accounting are often seen as more professionally managed, which can lead to better terms from lenders.

Challenges of accrual accounting

Despite its advantages, accrual accounting also comes with certain challenges:

- Complexity: Requires more robust accounting systems and expertise.

- Cash flow tracking: Since it doesn’t reflect cash movements directly, businesses must pay close attention to cash flow separately.

- Risk of misstatement: If not effectively managed, there is a risk of misstating revenue or expenses, especially around period-end.

- Initial setup: Transitioning from cash to accrual basis may require a more adept accounting system.

- Ongoing maintenance: Accrual accounting demands more frequent reconciliations which can take up the time of your accountants.

When should you use accrual accounting?

Businesses that meet any of the following criteria typically benefit from using accrual accounting:

- Annual revenues exceed a specific threshold (e.g., $25 million in the U.S. for tax purposes).

- Maintain inventory.

- Seek to raise investment or obtain credit.

- Need to comply with external financial reporting standards.

- Operate across multiple accounting periods with complex billing cycles.

- Provide services or products on credit.

Small businesses may choose cash basis accounting for simplicity unless regulatory bodies say differently. However, growing companies often switch to accrual accounting to enhance their reporting accuracy.

Industry specific applications of accrual accounting

Construction

In long-term construction projects, accrual accounting allows for the use of percentage-of-completion accounting, where revenue is recognized based on project completion. This provides a more accurate representation of project margins and performance over time.

Software as a Service (SaaS)

SaaS companies often sell annual or multi-year subscriptions. Accrual accounting ensures revenue is recognized monthly over the service period, not all at once when payment is received. It also allows for the recognition of deferred revenue as a liability, which is then recognized as earned income over the contract period.

Retail and manufacturing

Businesses with inventory benefit from accrual accounting because it allows for the proper matching of cost of goods sold with related sales. It also supports inventory valuation methods such as FIFO (First-In, First-Out) or LIFO (Last-In, First-Out), which are important aspects of financial reporting and tax preparation.

Healthcare and legal services

Professionals who provide services over time or rely on insurance reimbursements benefit from accrual accounting, as it allows them to recognize revenue when services are performed and track receivables and payables more accurately.

Example: Accrual accounting for prepaids

Let’s look at a real-world scenario involving a mid-sized accrual basis company. The company signs a $60,000 contract in November to purchase a software subscription over six months, beginning immediately. The company pays the full amount upfront.

Under accrual accounting:

- The $60,000 is recorded as a prepaid upon purchase.

- Each month, $10,000 is moved from prepaid software to software expense. ($60,000 ÷ 6 months = $10,000)

This approach ensures that expense is recognized in the period when the service is delivered, even though the cash was paid at the beginning of the contract. Below breaks down the entries necessary for initial posting and then amortization of that amount for the subsequent months.

Initial recording of purchase of software:

Monthly entries to amortize prepaid software expense:

Monthly entries to amortize prepaid software expense:

Alternative scenario (cash basis):

Alternative scenario (cash basis):

- The full $60,000 would be recorded as software expense in November, potentially overstating expenses for that month and misrepresenting the company’s ongoing financial performance.

This comparison highlights why accrual accounting is preferred for tracking long-term agreements and for businesses that offer services across multiple periods.

Initial recording of purchase of software:

Example: Accrual accounting for accruals

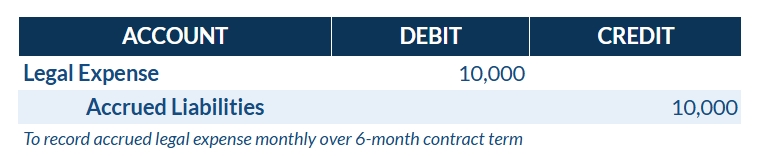

Let’s look at the same example but if it were an accrued expense. The company signs a $60,000 contract in November to obtain legal services over six months, beginning immediately. The company pays the full amount at the end of the contract when the terms are satisfied.

Under accrual accounting:

- The $60,000 is recorded as an accrued expense over the contract term.

- Each month, $10,000 is recorded as a legal expense with an associated accrued liability.

This approach once again ensures that expense is recognized in the period when the service is delivered, even though the cash was paid at the end of the contract. Below shows the entries necessary for accruing the expense and then the removal after payment is made.

Monthly entries:

Recording of cash payment and removal of accrual:

Recording of cash payment and removal of accrual:

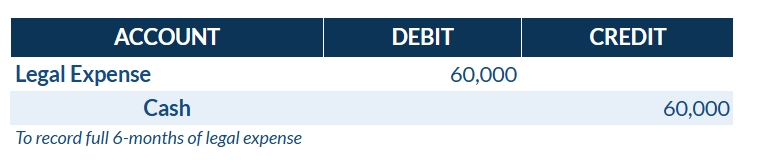

Alternative scenario (cash basis):

Alternative scenario (cash basis):

- The full $60,000 would be recorded as legal expense in April, at the end of the contract term.

Initial recording of legal fees:

This comparison effectively demonstrates why accrual accounting is preferred for tracking long-term agreements.

Summary

Accrual accounting allows businesses to accurately portray their financial performance and position. By recognizing revenues and expenses when they occur rather than when cash is exchanged, financial statements are more reflective of the company’s current position. Prepaids and accruals are the primary pieces of this method, allowing for the proper expense and revenue recognition. Although accrual accounting may be more complex and take some more effort, the benefits of accurately reporting the company’s position is likely worth it.

For most growing businesses, transitioning to accrual accounting is a move toward more professional and effective financial reporting.

It is essential for all current and future accountants to understand the different methods of accounting, especially the primary method for most companies.