Interest rates under ASC 842

The Financial Accounting Standards Board (FASB) issued ASC 842, Leases, in order to standardize financial reporting for companies with leases who report under US GAAP. One of the many goals of the FASB with the issuance of this new lease accounting standard was to enhance transparency into the true obligations arising from operating leases, through the recognition of a lease liability. Under previous standards, operating leases were off-balance sheet obligations, recognized as operating expenses throughout the term of the lease with no presence on a company’s balance sheet.

Under ASC 842 lessees must recognize a lease liability for all in-scope operating leases, and the lease liability must be calculated by taking the present value of the lease payments. Consequently, companies who may have only used discount rates for capital leases in the past must obtain discount rates for a significant amount of their existing lease portfolio, as well as for new leases. This creates the additional challenge of determining which discount rate to use, as it is rarely defined in the individual lease agreement and companies have many different options available per the guidance.

Because the lease’s discount rate directly impacts the classification of the lease and the initial valuation of the lease liability, which in turn directly impacts the corresponding right-of-use (ROU) asset, a company’s elections regarding their discount rates can have a significant impact on their balance sheet. This article will discuss the interest rate options available to lessees under ASC 842 and the implications and applications of each.

Implicit rate

Although this article will cover the various discount rate options available to lessees under ASC 842, it is important to first note that the implicit rate should be used before any other rate if it is readily available or can be accurately calculated. This is explicitly stated in ASC 842, specifically in 842-20-30-3: “a lessee should use the rate implicit in the lease whenever that rate is readily determinable.”

ASC 842 defines the implicit rate as the rate of interest that at any given date causes the aggregate present value of:

- The lease payments and

- The amount the lessor expects to derive from the underlying asset at the end of the lease term

to equal the sum of both

- The fair value of the underlying asset minus any related investment tax credits retained and expected to be realized by lessor and

- Any deferred initial direct costs of the lessor.

This definition is shown below as a formula:

Application of the implicit rate

Generally speaking, the implicit rate is the inherent rate of return the lessor is receiving from the lease, and is therefore not usually specified in the contract (i.e. implicit). As a lessor, this rate is readily available because the lessor drafts the lease agreement, thus knowing the required inputs to calculate the rate.

Due to the nature of the implicit rate, the lessee will rarely be privy to all of the required assumptions for the calculation, as this is ultimately the basis for the lessor’s profit margin on the lease. This means the rate would not be “readily determinable” by the lessee. For a detailed example of calculation and further explanation of the implicit rate, click here.

Although it can rarely be calculated by the lessee, one benefit of using the implicit rate is that for leases with fixed payments in which the lessee and lessor have similar credit ratings, the implicit interest rate will generally be higher than the lessee’s incremental borrowing rate as the implicit rate reflects the lessor’s minimum profit on the lease. The benefit of using a slightly higher rate is that it will give the lessee a lower lease liability.

Despite the implicit rate often producing the lowest lease liability of the three discount rate options, it is more likely that lessees will use an alternative rate like their own incremental borrowing rate or the risk-free rate (private companies only) to calculate the initial value of the lease liability per ASC 842.

Incremental borrowing rate (IBR)

The incremental borrowing rate (IBR) is the interest rate all lessees are able to use when the implicit rate is not readily available or able to be calculated, as made clear by the continuation of paragraph ASC 842-20-30-3. This section of the guidance explicitly states “if the rate implicit in the lease is not readily determinable, a lessee uses its incremental borrowing rate.”

The glossary of ASC 842 goes on to define the incremental borrowing rate as the rate of interest a lessee would have to pay to borrow an amount equal to the total lease payments on a collateralized basis over a similar term in a similar economic environment. Think about this as the rate charged by your bank or financial lender to borrow an amount of money equal to the total lease payments over the lease term.

Application of the incremental borrowing rate

The incremental borrowing rate is calculated based on factors specific to the company and the contract such as credit rating, the underlying asset, the lease term, and the economic environment. Because this is an organization-specific calculation, your treasury department may be able to assist when provided with specific information such as the lease term, the specific company/entity/subsidiary involved in the lease agreement, etc. They may already have a process in place for obtaining such information. However, for many companies, establishing an efficient and repeatable process for obtaining rates that would be applicable for collateralized borrowings can present additional questions. For example, what can we use as collateral?

It is generally acceptable to use the underlying leased asset as collateral in determining the incremental borrowing rate. However, other forms of collateral can be used if they are comparable and acceptable by the lender. Generally the more liquid, the more acceptable the collateral.

The IBR is more commonly used by the lessee to calculate the lease liability than the implicit rate. However, it can be difficult and expensive to obtain IBRs for the various leases in an entity’s portfolio, especially for non-public entities that may not have information like comparable credit spreads readily available. In cases where a company’s treasury department is not equipped to establish these rates, companies may choose to engage with external firms that specialize in valuations, third party lenders, or other parties to get an accurate estimation of an IBR. This can significantly increase the cost associated with maintaining compliance with ASC 842.

No matter the method a company uses to determine their IBR for their leases, it is important to document the method, reasoning, and overall findings and discuss the conclusions with the external auditors.

Risk-free rate

Expedient option

As discussed above, for lessees, the rate implicit in the lease is not usually readily determinable. Further, it can often be complex and even costly (if engaging an outside party) to estimate the incremental borrowing rate. In order to alleviate the burden of ASC 842 for non-public entities, private companies are permitted to use a risk-free rate as the discount rate for their entire portfolio of leases, or, by class of underlying asset as determined by the FASB amendment in 2021, for which they are acting as the lessee.

The risk-free rate is the rate investors expect to earn from an investment that carries zero risk over a period of time, such as a government treasury bill. The final portion of 842-20-30-3 also states that the risk-free rate should be determined using a period comparable with the lease term.

Application of the risk-free rate

The risk-free rate is by far the easiest rate to determine under ASC 842. Rather than requiring complex calculations or research, the risk-free rate can simply be found online on the treasury website.

While this alternative minimizes the work and potential costs associated with evaluating discount rates for a private company with a large lease portfolio, the risk-free rate is often the lowest of the three discount rate options. When calculating the lease liability, the lower risk-free rate can cause a materially higher lease liability for private companies. To address this, the FASB amendment from 2021 allows for non-public companies to apply the risk-free rate by class of underlying asset, rather than at the entity-wide level. If a company elects this policy, they must disclose which asset classes it has elected to apply a risk-free rate to. Additionally, when the rate implicit in the lease is readily determinable for any individual lease, the lessee must use that rate (rather than the risk-free rate or the IBR), regardless of whether it has made the risk-free rate election.

A final consideration when applying the risk-free rate is a company’s likelihood of going public. As the risk-free rate is only available to non-public entities, once a decision to go public is made, the entity must retrospectively eliminate the use of the risk-free rate from its historical financial statement prior to its IPO registration.

Proposed FASB amendment

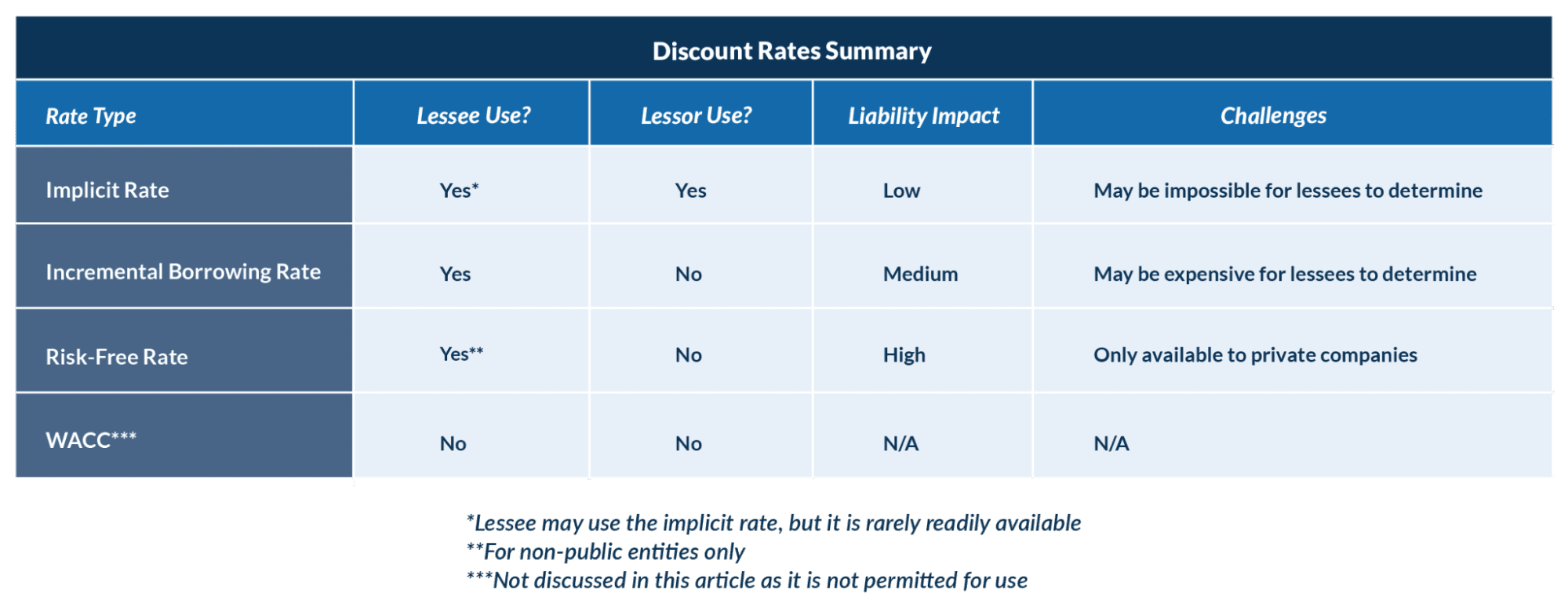

Below is a summary table comparing the different types of interest rates:

Summary

While a foolproof way to discern the discount rate for a lease does not exist, knowing the different options available and how to apply them correctly can help ease the burden of initial and ongoing compliance with ASC 842. Though the implicit rate should be applied when readily determinable by the lessee, this is rarely the case, and the standard has provided guidance allowing the application of the IBR or the risk-free rate (for non-public entities only).