In the landscape of accrual accounting, the correct classification of short-term obligations is fundamental to maintaining the accuracy of a company’s financial reporting. While both accrued expenses and Accounts Payable (AP) represent liabilities for goods or services received by a company but not yet paid for, they are distinguished by their recognition timing and the certainty of their valuation.

What are accounts payable?

Accounts payable represents a company’s invoiced debts to vendors, or more specifically, the obligation to pay for goods or services that have been received from vendors on credit. The defining characteristic of AP is the receipt of an invoice.

Key characteristics of accounts payable

Under the accrual method, an accounts payable entry is triggered when the control of goods transfers to the buyer or when a service is rendered, provided an invoice has been processed through the procurement cycle.

- Documentation: Supported by a vendor invoice, purchase order, and receiving report/goods receipt (the “three-way match”).

- Timing: Accounts payable are recorded by a company once they get an invoice to pay for goods or services.

- Valuation: The amount is typically fixed and determined by the contractual terms stated on the invoice from the vendor.

What are accrued expenses?

Accrued expenses (also known as accrued liabilities, sometimes referred to as AP accruals) refer to expenses that have been incurred during an accounting period but for which no invoice has been received or no payment is due by the accounting period close date. The recognition of accrued expenses is essential to ensure that all of a company’s expenses for services received are recognized in the period they occur, regardless of whether an invoice was received or a payment was made, adhering to the matching principle.

Key categories of accruals

Unlike accounts payable, accrued expenses often require a degree of estimation or calculation, (and ultimately may be trued up once actuals are realized), based on various methods or data points, such as historical data, contractual obligations, or even vendor confirmations.

While some accrued expenses eventually flow through the AP process as external vendors/suppliers have provided a service and eventually a corresponding invoice will come in (AP accruals), some accrued expenses will never have an external invoice flow through AP, as they are internal calculations as “other accrued liabilities”.

For example, unbilled products and services such as utilities, consulting services, usage based cloud services, advertising, and other vendor services would be vendor accruals that eventually flow through AP, (AP accruals) while other accrued liabilities would include accrued taxes, accrued bonuses, wages and salaries, interest, etc.

- Nature of Expense: Includes unbilled products and services such as utilities and usage based services, as well as internal wages, bonuses, interest, and taxes.

- Valuation: Internally calculated and adjustments journal entries recognized at the end of the accounting period.

- Timing: Accrued expenses are captured at the end of the accounting period to recognize the expenses that have been incurred but not yet invoiced or paid. They are typically reversed during the expected invoice/payment due period to avoid double-counting once the actual invoice arrives or the payment is made.

Compared to AP, auditors scrutinize accrued expenses more heavily because accrued expenses are susceptible to management bias or “earnings smoothing” due to the estimation involved. Organizations should have internal controls in place to ensure that accrual estimates are based on verifiable data, such as utility meter readings or unbilled hours from service providers.

Example: Consulting services, from accrued expenses to accounts payable

A common vendor accrual example is for consulting services, so let’s assume Company A engages with a third party for services on October 1st based on an hourly rate of $100 per hour to work on a project that is estimated will take 60 hours of consulting services, for a total estimated cost of $6,000, with the project completed by December 31st. The consulting company will send them an invoice at the end of the quarter for the work actually completed, to be paid in arrears, with Net 30 payment terms (which means the full payment is due 30 days after the invoice date.) On October 31st, Company A estimates that they have used 1/3rd of the allotted 60 hours, so an entry would be made for the following accrual, for 20 hours x $100 per hour:

For the simplicity of our example, let’s assume entries for November and December are also booked for the remaining $2,000 for each month, and therefore, on December 31st, Company A would have $6,000 of accrued consulting expense and $6,000 of accrued liabilities to close out the year.

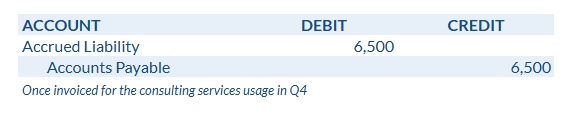

Come January 15th, Company A receives the invoice for the Q4 consulting services. On the invoice, the consulting company says that 65 hours were actually provided to the client for consulting services throughout the quarter. At that time, Company A would make the following entry to adjust for the missing 5 hours of accrued expense:

Additionally, an entry is made to move the full accrued liability balance for the consulting accrual into accounts payable, to clear out everything that was previously accrued for:

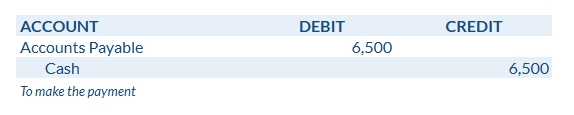

It takes some time to process the payment through AP, so the actual payment isn’t made until January 17th. At that time, the entry is made for the following:

The following table outlines the primary differences between Accounts Payable and Accrued Expenses:

| Feature | Accounts Payable | Accrued Expenses |

|---|---|---|

| Triggering Event | Receipt of vendor invoice. | Consumption of benefit/passage of time. |

| Certainty | High; based on explicit billing. | Moderate; may require management estimation. |

| Primary Document | Vendor Invoice. | Internal worksheets/contracts/timecards. |

| Payment Timing | Typically short-term (30–90 days). | Variable |

Summary

In summary, while accrued expenses and accounts payable both represent current liabilities, their distinction lies in the timing throughout the billing cycle. Accounts payable is the recognition of a company’s payment obligation(s) backed by a formal invoice, while accrued expenses represent the proactive recognition of costs incurred but not yet billed. Understanding and recognizing these distinctions leads to more accurate reporting, ultimately providing a true reflection of an entity’s financial obligations and operational expenses.