Accrual accounting is a pivotal component of financial reporting, as it is necessary for organizations that adhere to Generally Accepted Accounting Principles (GAAP). This is a means of ensuring an organization is properly tracking when events actually occur, not when cash changes hands. When it comes to accounting for taxes, accrual accounting is crucial for accurately depicting profitability.

The goal of properly accounting for taxes on an accrual basis is simple: to ensure the tax expense is matched to the income or activity that generated it, regardless of the payment schedule set by the taxing authority. This article focuses on the mechanism of accrued taxes—a key element in achieving this accuracy—while briefly touching upon its counterpart, prepaid taxes.

Matching principle and accruals

Under GAAP, specifically following guidance in resources like FASB ASC 740, Income Taxes, businesses must recognize the tax consequences of events in the same period those events are recognized in the financial statements. This is the matching principle in action.

What are accrued taxes?

Within the concept of accruals, an accrued tax is an obligation normally set in the future created by an economic event. While this obligation has been incurred, it has not yet been paid and will be accounted for as a liability for the business.

- Key concept: The company has earned taxable income or engaged in an activity (like utilizing property or paying employees) that legally obligates it to pay a tax, but the official payment date is at a later period.

- Financial statement impact: Accrued taxes are recorded as a liability on the Balance Sheet, typically under the line item taxes payable. On the income statement, the corresponding tax expense is recognized immediately.

Why accrue taxes?

Many organizations are required to make estimated tax payments quarterly for income tax, or they may have annual obligations for property taxes. Accrual ensures:

- Accurate profitability: The expense is captured in the period the income was earned, providing a true Net Income figure.

- Compliance: Adherence to GAAP, which is essential for external reporting, lending, and auditing.

- Cash flow management: Management has a clear picture of future cash outflows, even if the payment deadline is months away.

Estimating taxable amount and straight-line expense recognition

Generally, in practice, the tax amount is an estimation and the expense is straight-lined on a go forward basis.

Estimating the tax liability

Organizations must proactively estimate their tax liability throughout the year based on anticipated results and the statutory tax rate. In this example, the estimated tax rate is 20%:

- Determine taxable income estimate: To begin, the business will look to determine probable taxable income for the full period (e.g., the year).

- Apply estimated rate: Management applies the relevant statutory tax rate (e.g., 20%) to this estimated income to project the total tax liability (tax expected to be owed).

- Calculate monthly accrual (straight-line): The business will take the estimated tax payment expected to be paid and straight-line it (i.e., divide the amount by the term). This allows them to appropriately spread the expense over the periods where income is earned.

This method ensures the tax expense is recognized uniformly as the underlying business activity takes place, preventing a large, unexpected expense hit in the month the payment is due.

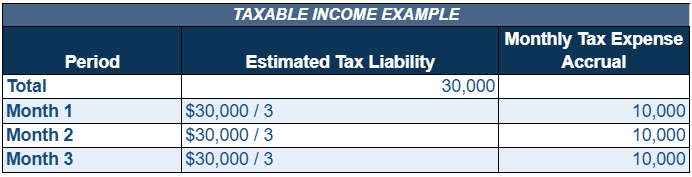

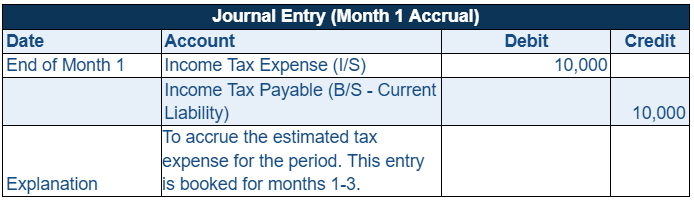

Example: Monthly income tax accrual

Assume an organization expects to accrue a total tax liability of $30,000 over the next quarter (3 months) based on its income forecast and estimated tax rate.

By the end of Month 3, the cumulative balance in the income tax payable account will be the estimated $30,000.

The reconciling act: The true-up

Estimates are just that, estimations of an expected amount. At the end of the reporting period or when the actual tax liability is confirmed, the estimated accrued balance must be trued-up (reconciled) to the actual, final amount.

Example: True-up

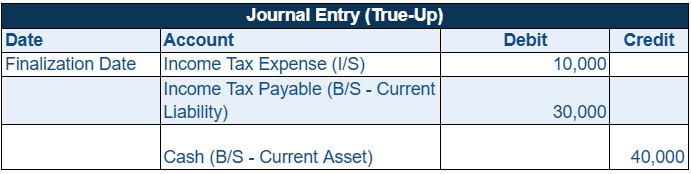

In this example, let’s say the final tax liability results in a final calculation of $40,000 (not the estimated $30,000).

- Current liability balance: The income tax payable account currently holds the estimated accrued balance of $30,000.

- Required true-up: The company must recognize the remaining $10,000 liability ($40,000 actual – $30,000 accrued). This additional expense is recognized in the period the final calculation is made.

When payment is made at the end of the quarter, we relieve the income tax payable accrual account for the $30,000 accrued over the quarter, and we expense the additional $10,000 immediately, as it represents an expense incurred during the previous quarter. From there, we credit Cash for $40,000 to account for the total payment, in accordance with the matching principle.

Briefly touching on prepaid taxes

While the focus is on accruals, it is necessary to contrast them with prepaid taxes to understand the full spectrum of tax timing issues.

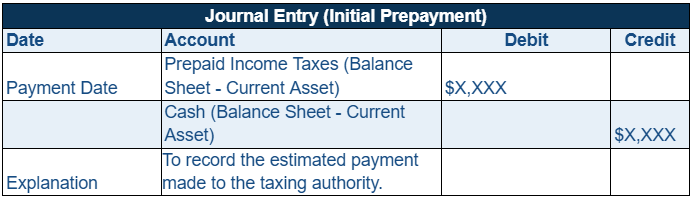

A prepaid tax is an asset created when a tax payment is made before the expense has been incurred.

- Nature: It is a current asset because it represents a future economic benefit—either in the form of a reduction of a future tax liability or a refund.

- Example: A business makes an estimated quarterly income tax payment based on its forecast. Since the true tax expense for the period hasn’t been finalized (incurred) yet, the cash paid is initially recorded as a Prepaid Tax Asset.

At the end of the period, when the actual tax expense is calculated, the prepaid tax asset is used to offset the tax payable liability. If the prepayment was too high, the remaining balance is a tax refund receivable; if too low, an additional amount is due (true-up).

In conclusion, managing accrued taxes is a crucial practice under the accrual basis of accounting. By systematically estimating, accruing, and ultimately truing up the tax expense and taxes payable accounts, an organization ensures its financial statements accurately reflect the economic reality of its operations, thereby adhering to GAAP’s fundamental principles.