1. The foundation: Accrual accounting and the matching principle

2. Understanding the full scope of accrued payroll

3. Examples: Bi-weekly pay and month-end accruals

4. Beyond basic wages: Commissions and bonuses

5. Why a software system is non-negotiable

Have you ever wondered what happens behind the scenes in a company’s accounting department between paychecks? While you might get paid every two weeks, the company’s financial records need to be up-to-date. This is where payroll accruals come in, and understanding them is crucial for a company’s financial health.

At its core, an accrual is a financial placeholder for an expense a company has incurred but hasn’t yet paid. Think of it like this: You use your phone for a full month, but the bill doesn’t arrive until the next one. The cost of that phone usage is an accrued expense—an obligation that exists because you’ve already received a service.

The same principle applies to payroll. As an employee, you earn compensation for every day you work, which creates a financial obligation for your employer. This obligation—the money you’ve earned but haven’t been paid for yet—is an accrued wage or accrued salary. This practice is essential for maintaining financial accuracy and transparency.

The foundation: Accrual accounting and the matching principle

The concept of accrual accounting is best understood by contrasting it with cash accounting. The key difference is the timing of when financial transactions are recorded.

- Cash Basis Accounting: This method records revenues and expenses only when cash physically changes hands. While it’s simpler, it can present a distorted view of a company’s profitability because it doesn’t match expenses to the period in which they were incurred.

- Accrual Basis Accounting: This method, mandated for most large and publicly traded companies under US GAAP, records revenues when they’re earned and expenses when they’re incurred, regardless of when cash is exchanged. It provides a more accurate picture of a company’s long-term financial health.

At the heart of accrual accounting is the matching principle. This principle requires a company to record expenses in the same period as the revenues those expenses helped generate. For payroll, this means the cost of labor must be recorded in the same period the work was performed, even if payday happens in a different month. This ensures the company’s financial statements accurately reflect the full cost of labor required to generate revenue.

Understanding the full scope of accrued payroll

Accrued payroll is a comprehensive term that goes beyond just base pay. It includes a wide range of a company’s financial obligations to its employees:

- Wages and Salaries: The most significant component of this is the compensation earned by hourly and salaried employees for work that hasn’t yet been paid.

- Commissions and Bonuses: Any incentive-based pay earned by an employee is included, as it represents an obligation for services already rendered.

- Paid Time Off (PTO) and Vacation: The value of earned but unused PTO or vacation time must be accrued as a liability when unused time can be carried forward to later periods.

- Employer-Paid Payroll Taxes and Contributions: The employer’s portion of payroll taxes (like Social Security and Medicare) and contributions to benefits (like health insurance) are also accrued.

Examples: Bi-weekly pay and month-end accruals

A common situation that requires a payroll accrual is when a company’s pay schedule doesn’t align with its accounting period. Let’s look at a consistent example across different scenarios:

Example 1: Understanding accrual journal entry

Scenario: Your company’s accounting period ends on December 31st. Employees are paid bi-weekly on Fridays. The last payday of the year was Friday, December 26th. Even though employees have worked for three days (December 29th, 30th, and 31st), they won’t be paid for that work until the next payroll run on Friday, January 9th.

To ensure the financial records for December are accurate, the accounting team must perform a journal entry to record the liability for the work performed on December 29th, 30th, and 31st.

The journal entry in action

Let’s assume the total wages for those three days amounted to $3,000 for all employees.

- December 31st (Initial Accrual Entry)

- Debit: Wages Expense $3,000 – This increases the company’s expense account for work performed in December.

- Credit: Accrued Wages Payable $3,000 – This increases the company’s liability account, showing the amount owed to employees.

- January 9th (Payment and Reversal Entry)

- When the employees are paid, the company makes a reversing entry to clear the liability.

- Debit: Accrued Wages Payable $3,000 – This clears the accrued liability from the balance sheet.

- Credit: Cash $3,000 – This reflects the cash outflow for the payment.

This two-part process ensures that financial statements aren’t distorted by the timing difference between when an expense is incurred and when it is paid.

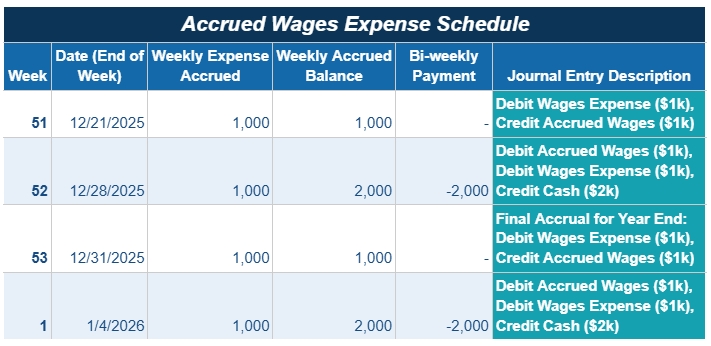

Example 2: Visualizing the accrual schedule

To make this example even clearer, here is a simplified table showing how the weekly expenses and payments would be tracked. For this example, let’s assume a single employee earns a bi-weekly salary of $2,000. Each week accrues an expense of $1,000, and a payment of $2,000 is made every two weeks.

Note: For the final week of the year, a special accrual is performed to capture the last few days of work that will be paid in the next year.

Beyond basic wages: Commissions and bonuses

The accrual principle also applies to other types of compensation, like commissions and bonuses, ensuring the expense is recognized when it’s earned.

Commission Example: A sales representative closes a major deal on December 29th, earning a $2,000 commission. The company’s policy is to pay commissions on the next payday, which is January 9th. To match the expense with the revenue from the sale, the company must accrue for the commission in December.

- December 31st Journal Entry

- Debit: Commission Expense $2,000

- Credit: Accrued Commission Liability $2,000

Bonus Example: A company’s year-end bonus program is based on performance in December, with a $5,000 bonus to be paid out on January 9th. The bonus is considered earned once the performance criteria are met. The company must accrue for this expense in December.

- December 31st Journal Entry

- Debit: Bonus Expense $5,000

- Credit: Accrued Bonus Payable $5,000

Why a software system is non-negotiable

For any organization, a reliable system for managing payroll accruals is essential. Manually tracking and calculating these entries for every employee is a significant risk, prone to errors that can lead to compliance issues and audit headaches.

A dedicated system automates this entire process, transforming a manual burden into a strategic advantage. It can:

- Calculate Accruals Instantly: It tracks wages, salaries, commissions, and other benefits in real-time, instantly calculating the exact accrued amount at the end of each accounting period. This eliminates the need for manual spreadsheets and guesswork.

- Ensure Accuracy and Compliance: By automating complex calculations, a software system drastically reduces human error, ensuring your financial records are consistently accurate and compliant with financial reporting standards.

- Provide a Clear Financial Picture: With a real-time, consolidated view of your liabilities, management gains a precise understanding of the company’s financial position. This empowers better decisions about budgeting, cash flow, and overall financial strategy.

The broader impact on financial statements

Accurate payroll accruals directly impact a company’s core financial statements, providing a truthful representation of its financial health.

- On the Balance Sheet: Accrued payroll is recorded as a current liability, an obligation that is expected to be settled within one year. This gives stakeholders a clear snapshot of the company’s short-term financial obligations at a specific point in time.

- On the Income Statement: The corresponding debit is recognized as an expense on the income statement, where the company’s true profitability is displayed. By recording the payroll expense in the period the labor was performed, it is matched with the revenues generated in that same period, providing an accurate view of performance.

In essence, accrued wages and other payroll liabilities are a fundamental pillar of financial integrity and sound business management. By recognizing expenses when they’re incurred—not just when they’re paid—businesses transform raw financial data into a powerful tool for strategic decision-making and sustainable growth.