Lessee vs lessor accounting

Government entity lessees reporting under GASB are required to recognize a lease liability and related lease asset at the lease commencement date, or the transition date to GASB 87, if commencement is prior to transition. The lease liability is equal to the present value of the expected lease payments over the lease term. The related lease asset is equal to the lease liability with a few minor adjustments.

Lessors under GASB 87 are required to record a lease receivable and deferred inflow of resources at the commencement of the lease term. As with the lease liability for a lessee, the lease receivable is calculated as the present value of the remaining lease payments expected to be received during the lease term. The deferred inflow of resources is treated similarly to deferred revenue and is equal to the lease receivable with a few minor adjustments.

The changes to lessor accounting under GASB 87 are the result of mirroring lessee accounting. Where lessee accounting recognizes a lease liability equal to the present value of the expected future lease payments, lessor accounting recognizes a lease receivable, calculated similarly from expected receipts. Conversely, lessee accounting also requires the recognition of the leased asset derived from the lease liability, whereas lessor accounting records the deferred inflow of resources as a derivative of the lease receivable.

Lessor accounting under GASB 87

As a lessor reporting under GASB 87, the initial journal entry to record a lease on the commencement date or transition date for an existing lease establishes a lease receivable and a deferred inflow of resources. The lease receivable is measured at the present value of lease payments expected to be received during the lease term. The deferred inflow of resources is measured as the lease receivable balance adjusted for prepayments received or incentives paid. Specifically, the lessor will add prepayments received from the lessee and subtract any lease incentives paid to the lessee at or before lease commencement from the lease receivable calculation to determine the initial value of the deferred inflow of resources.

During subsequent months, the lessor records the receipt of cash payments and recognizes interest revenue and a reduction to the lease receivable in accordance with the amortization table. Additionally, the lessor recognizes lease revenue calculated as the straight-line amortization of the deferred inflow of resources over the lease term.

An example of lessor accounting for a lease under GASB 87

The comprehensive example below will illustrate the accounting treatment of a lease from a lessor’s perspective under GASB 87. This scenario shows the calculations and journal entries to account for a lease arrangement under GASB 87 on the commencement date, the first month of the lease term, and subsequent months.

We will assume the following lease terms and background information in our example of a building lease from the perspective of the lessor:

- Possession Date: January 1, 2022

- Date of Transition to GASB 87: January 1, 2022

- Lease End Date: December 31, 2026

- Base Rent Payment: $10,000/ month (due on the last day of each month)

- Lease Incentive: $10,000 paid on January 1, 2022

- Discount rate: 2%

Initial recognition

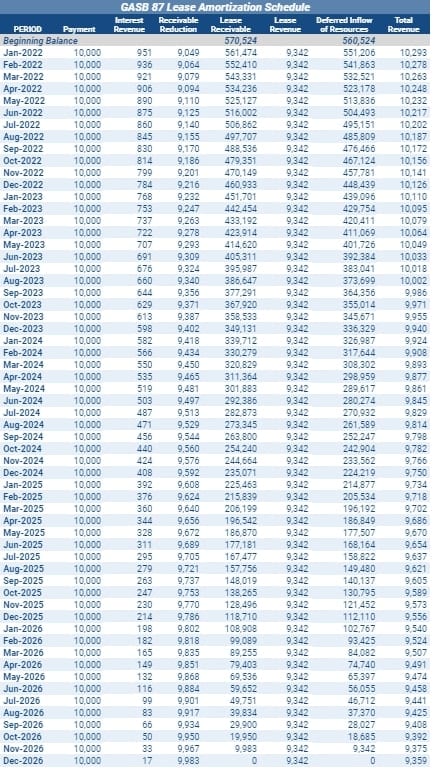

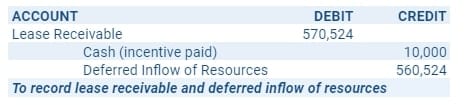

The present value of the remaining lease payments at lease commencement, discounted at the 2% rate, is $570,524. In this example, an incentive was paid by the lessor to the lessee on the lease commencement date. Therefore, the incentive payment of $10,000 is subtracted from the lease receivable balance to calculate the deferred inflow of resources at lease commencement. After adjusting for the incentive paid to the lessee, the deferred inflow of resources is calculated to be $560,524. Below is the amortization table of the lease receivable at the discount rate and the corresponding deferred inflow of resources:

Initial journal entry

The entry to record the lease at commencement is a debit to establish the lease receivable of $570,524, a credit to establish the deferred inflow of resources of $560,524, and a credit to cash of $10,000 to represent the incentive paid to the lessee at commencement.

Subsequent journal entries

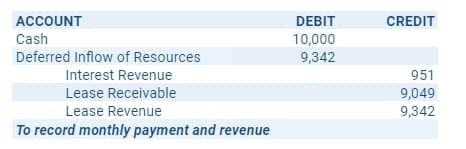

At the end of January, interest revenue is calculated at the discount rate times the beginning of the month lease receivable balance times the number of days in the month. In this example, the calculation for interest revenue in January 2022 is as follows: Divide the 2% discount rate by 12 months to calculate the monthly rate of interest. Multiply the monthly interest rate by the beginning receivable balance of $570,524 to arrive at $951 (2% / 12 months x $570,524) of interest revenue for the month.

The credit, or reduction of, the lease receivable is the difference between the cash received and interest revenue. In this example, the calculation of the January 2022 lease receivable reduction is as follows: The cash receipt of $10,000 minus interest revenue of $951 equals a receivable reduction of $9,049.

As lease revenue is recognized on a straight-line basis, this reduces the balance of the deferred inflow of resources. Therefore in January 2022, the applicable lease revenue is calculated by dividing the beginning deferred inflow of resources balance by the number of months in the lease term ($560,524 / 60 months = $9,342), resulting in a monthly recognition of lease revenue and amortization of deferred inflow of resources. The combined entry for January 2022 is as follows:

In later months a similar entry will be recorded, with the interest revenue and lease receivable reduction amounts changing as the lease receivable decreases with periodic payments.

GASB 87 RFP template

Are you considering lease accounting software for your GASB 87 lessor leases? Our RFP template will make the software comparison process easier.

Summary

We provided a conceptual overview and step-by-step example of the accounting treatment of leases for lessors under the new accounting standard. If capturing the activity within the governmental fund, a conversion entry will be necessary at year-end to convert from the modified accrual accounting basis to the required full accrual basis for the government-wide financials.

The recognition of a lease receivable and a deferred inflow of resources is a new concept under GASB 87 meant to mirror lessee accounting. Any change to accounting can present challenges if organizations are not prepared to report under the new accounting requirements. However, advanced knowledge of the change and understanding of the drivers to change can lead any organization successfully through a transition.

As shown in the article, the accounting for lessors under GASB 87 is complex. If you have further questions or concerns you can remove all room for doubt with cloud-based lease software for GASB 87 built by accountants. LeaseQuery is dedicated to providing a software solution best suited to handle the complexities of GASB 87 lease accounting. Schedule a demo with us today and see how the system will ensure your compliance with the new standard.