In this segment, the focus will be on how to account for distributions in excess of carrying value. For a refresher on the principles of equity method accounting, please see this article: The Equity Method of Accounting for Investments and Joint Ventures under ASC 323. Additionally, for further information regarding the recognition of losses in excess of the carrying value, please see Accounting for Loss from Equity Method Investments.

Equity method

The equity method of accounting applies when an organization invests in a company and exercises significant influence, but does not control the company. Equity investments in a separate entity can be held in the form of common stock of a corporation, or a capital investment in partnership, joint venture, or limited liability company. For the equity method of accounting to apply to the investment, the investor must have the ability to influence the operating and financial decisions of the investee.

Per ASC 323, the equity method of accounting is applicable to the following types of investments:

- Common stock

- In-substance common stock

- Capital investment

- Undivided instruments

Accounting for distributions exceeding carrying value

Per ASC 323, the investor measures the initial value of an equity method investment at cost, recording the investment as an asset offset by the consideration exchanged. The value of the investment is increased periodically by the investor’s proportionate share of the investee’s current period net income. On the other hand, the investment is decreased periodically by the investor’s portion of the investee’s current period net loss, distributions, and dividends.

An investor recognizes dividends and distributions as reductions to the carrying amount of an investment as long as the investment has a balance greater than zero (i.e., a debit balance). If the investment balance has been reduced to zero (either due to cumulative equity losses or dividends/distributions received), then any subsequent distributions received should not further reduce the investment balance. In other words, distributions should not result in a negative investment balance.

To account for distributions and dividends received when the investment balance is at or below zero, the investor has two options. These options are discussed in further detail in our example below.

- Option 1: Record the excess distribution as a gain

- Option 2: Record the excess distribution as a liability

Additionally, if the investment balance has been reduced to zero as a result of distributions or dividends, the investor stops recognizing its share of equity earnings and losses until cumulative future earnings exceed the excess distributions/dividends received. It is important to note this approach is similar to when investee losses are in excess of the investment balance. In both approaches, the investor must continue to track equity earnings and losses even though they are not recorded in order to determine when the investment balance is brought back to zero and the equity method of accounting is resumed.

Cash flow classification

The investor presents equity in earnings as an adjustment to its net income when arriving at the net cash flow from operations. However, when an investor receives a distribution from the investee, the investor must decide whether the distribution is a “return on”, or a “return of” investment. The decision impacts the cash flow classification:

- Returns on investment are cash flows from operating activities

- Returns of investment are cash flows from investing activities

The investor may elect one of two approaches to determine whether the distribution is a return on or a return of investment. The two approaches are:

- The cumulative earnings approach

- The nature of distribution approach

Cumulative earnings approach

If an investor elects the cumulative earnings approach, cumulative distributions received up to the total cumulative equity in US GAAP earnings is a return on investment. These distributions are classified as cash flows from operating activities.

Distributions exceeding the total cumulative equity in US GAAP earnings represent a return of investment and are classified as cash flows from investing activities.

Nature of distribution approach

If an investor elects the nature of distribution approach, cash flow classification is made for each individual distribution based on various factors, or the nature of the distribution. One factor to consider is whether the distribution was the result of the investee’s normal course of business. These distributions would likely be treated as cash flows from operating activities. On the other hand, distributions as a result of operations outside the normal course business would likely be treated as cash flows from investing activities.

Example: Accounting for an equity method investment when distributions exceed the carrying value

The scenario outlined below illustrates the required calculations and journal entries necessary to correctly account for an equity investment with distributions exceeding the carrying value of the investment.

For this example let’s assume Company A initially purchases stock in Company Z equating to a 25% ownership in Company Z for a purchase price of $500,000. Company A’s 25% ownership provides them significant influence over the operational and financial decisions of Company Z. Therefore, Company A records their investment in Company Z using the equity method of accounting.

Initial measurement

Company A records the initial value of their equity investment at cost as a debit to an investment account and a credit for the cash payment. The investment is recorded in the period the transaction is made with the following journal entry:

Subsequent measurement

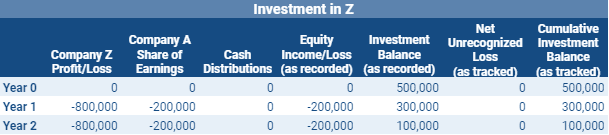

In the first two years of operation, Company Z incurred losses each year of $800,000. As a result of Company A’s 25% ownership in Company Z, they must recognize $200,000 ($800,000 x 25%) of loss each year.

Year 1

Year 2

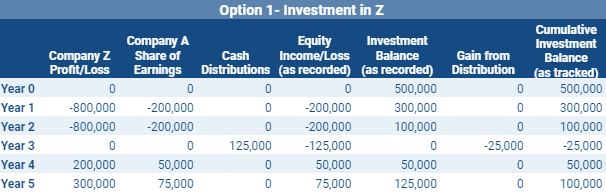

At the end of year two, the remaining investment balance in Company Z is $100,000, as illustrated in the table below:

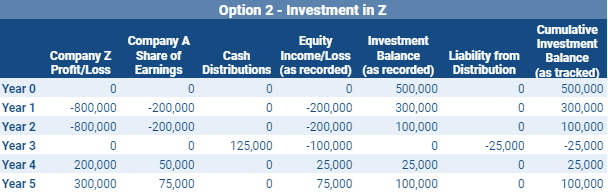

Year 3

In year three, Company Z records no profit or loss, but declares a cash distribution of $500,000. Company A’s portion of the distribution is $125,000 ($500,000 x 25%). Dividends received by an investor reduce the carrying balance of the investment. In this example, the amount of cash distribution exceeds the existing investment balance ($125,000 > $100,000). Therefore, Company A can record the excess distribution using either of the following options:

- Option 1: Record the excess distribution as a gain

- Option 2: Record the excess distribution as a liability

Company A should use careful consideration when determining which accounting treatment is appropriate for their specific circumstances. The following factors should be considered when making this determination:

- Implicit or explicit commitments to fund Company Z

- The source of the distributions

- Whether or not the distributions are refundable

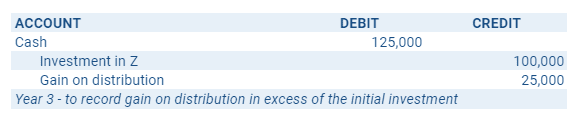

Option 1: Record the excess distribution as a gain

This accounting treatment should be used if Company A is not liable for the financial obligations of Company Z. The excess distribution of $25,000 ($125,000 – $100,000) is recorded as a gain with the receipt of the cash distribution:

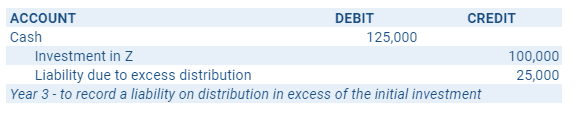

Option 2: Record the excess distribution as a liability

Option 2: Record the excess distribution as a liability

In this approach, Company Z is deferring the gain recognition of the $25,000 excess distribution by recording a liability.

Year 4

In year four, Company Z records a total profit of $200,000. Company A’s proportionate share of income is $50,000 ($200,000 x 25%). Therefore, during year four Company A receives income from their investment in Company Z of $50,000. The different entries under option 1 and option 2 for the recognition of the income are shown below.

Option 1:

Company A records the amount of equity income exceeding the previously recognized gain on distribution, or $25,000 ($50,000 – $25,000). However, if the earnings were less than the $25,000 gain previously recorded, Company A would have suspended recording any subsequent equity earnings until accumulated earnings equaled and then surpassed the aggregate gain recorded.

Option 2:

Option 2:

Under option 2, Company A initially deferred the gain and established a liability of the excess distribution amount of $25,000. In this scenario, Company A’s portion of equity earnings of $50,000 exceeds the liability by $25,000 ($50,000 – $25,000). Therefore Company A will relieve the liability of $25,000, recognize its full share of equity income, and record the remaining amount to the investment account.

Year 5

During the fifth year of operation Company Z records earnings of $300,000. Company A’s proportionate share of the earnings is $75,000 ($300,000 x 25%). No deferred gains or cumulative losses remain to offset the income under either accounting treatment option, and as such, Company A records its full portion of the income from its investment in Company Z:

Full Example

Below are two tables displaying the accounting treatment under both option 1 and option 2:

Option 1- Record excess distribution as a gain

Option 2 – Defer gain and recognize a liability from distribution

Summary

This article discussed how to account for distributions and dividends in excess of equity investment balances, as outlined in ASC 323 Investments – Equity Method and Joint Ventures. In summary, after the initial investment is recorded, the value of the investment is decreased by distributions and dividends received. If an investment balance will be reduced to below zero as a result of received distributions, the investor will have two options to account for the excess distribution. The options are to either record the excess distribution as a gain, or to record the excess distribution as a liability.

If the excess distributions are recorded as a gain, subsequent equity earnings are not recognized until the gain is fully offset. However, this is not the case if the excess distributions are recorded as a liability. Instead the full equity earnings are recognized, offset by relieving the liability first, followed by increasing the investment balance with any remaining or subsequent equity earnings.

This was one part of our equity method series. Stay tuned for additional articles further discussing specific and increasingly complex scenarios and examples under equity method accounting.