Equity method of accounting when basis differences exist

The equity method of accounting, which is governed by ASC 323 Investments — Equity Method and Joint Ventures (“ASC 323”), is used to account for an entity’s investment in another entity when it holds significant influence over the investee but does not fully control it. Generally, an investor is considered to have significant influence over the investee and should apply the equity method of accounting when it holds an ownership interest between 20% to 50%. However, US GAAP does not set bright lines for determining when an investor has significant influence and in reality making this conclusion requires careful analysis and judgment.

Once an entity has concluded that the equity method of accounting is appropriate, the next step is to record the investment at its initial cost. ASC 323 specifies that an investor should initially measure its equity method investment at cost in accordance with the guidelines in ASC 805 Business Combinations (“ASC 805”). In addition, an investor must identify any differences between the cost basis of its investment and its proportionate share of the underlying assets and liabilities as recorded by the investee. These differences are referred to as basis differences and must be accounted for by the investor as if the investee were a consolidated subsidiary even though its equity method investment is presented as a single line item on the balance sheet.

Sometimes the initial measurement and analysis of basis differences is straightforward, such as in the case when multiple investors contribute only cash to form a new joint venture. In this example, the underlying net assets balance of the new joint venture is made up entirely of cash and, as such, each investor’s proportionate share of the joint venture’s assets will equal the amount of cash contributed and no basis differences exist. However, what happens when an investor purchases an investment in an existing entity that has multiple assets and liabilities recorded at carrying value?

This article will discuss how to identify and account for basis differences of an equity method investment in accordance with ASC 323 and will use a hypothetical example to illustrate the appropriate accounting treatment.

What are basis differences and how do you identify them?

When purchasing an equity method investment in an investee entity, an investor generally acquires a share of that investee entity’s underlying assets and liabilities proportionate to its ownership interest. Since an investor’s purchase price in an orderly, arms length transaction is intended to represent the fair value of the investment, the consideration paid by an investor frequently does not match its proportionate share of an investee’s net assets, which are generally recorded at book value rather than fair value.

ASC 805 requires an investor to incorporate all consolidation-type adjustments and apply the acquisition method of accounting to its equity method investment similar to what it would do if it acquired a consolidated subsidiary. However, an investor’s equity method investment balance is presented on a single line item of the balance sheet. This presentation is commonly referred to as “one-line consolidation.” This means an investor must determine the acquisition date fair value of the identified assets and liabilities, which might include identifying intangible assets not already recorded on the investee’s balance sheet. These fair values are then compared to the recorded balances in the investee’s balance sheet. Any differences between the assessed fair values and the recorded balances are considered basis differences and must be incorporated into an investor’s equity method accounting.

When these types of basis differences exist, an investor’s cost basis in an investee might exceed its proportionate share of the book value of the underlying net assets. This excess represents goodwill, which is often referred to as “equity method goodwill.” However, consistent with the acquisition method in ASC 805, an investor should not automatically allocate the excess entirely to goodwill but must first attribute the excess to fair value adjustments of the identified assets and liabilities. Any residual amount remaining after all assets and liabilities are properly identified is considered equity method goodwill. Equity method goodwill is not amortized (except for certain qualifying private entities that elect the accounting alternative in ASC 350 Intangibles — Goodwill and Other), but should be considered when performing an impairment analysis of the equity method investment.

To learn more about goodwill in accounting, read our article, “Goodwill in Accounting Overview: Definition, How to Calculate It, and More.”

How do basis differences impact equity method accounting?

Properly identifying and tracking basis differences is an important step in equity method accounting. An investor’s share of investee earnings must be adjusted to reflect these basis differences. For example, a common basis difference in equity method investments is the difference between the fair value of the investee’s fixed assets at the acquisition date and the book value recorded in the investee’s balance sheet. In this case, the investee’s reported earnings each period will reflect depreciation expense based on the existing carrying value, but an investor must also factor in the depreciation expense associated with the step-up in fair value that was identified at the acquisition date. If a company does not account for its basis differences, it could result in the misstatement of its equity method earnings.

Since equity method investments are presented on a single line of the balance sheet, it is important for an investor to accurately track basis differences and equity method goodwill in a separate subsidiary ledger, often referred to as “memo” accounts.

An example of equity method accounting with basis differences

To illustrate the impact of equity method basis differences and how to properly account for them, we will use the following example. Note that this example ignores income tax impacts for simplicity.

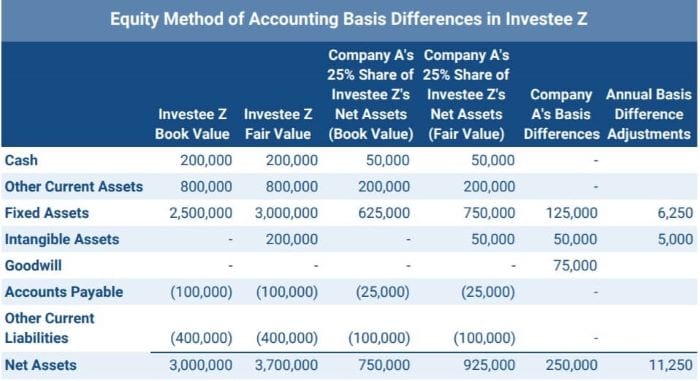

On January 1, 2020, Company A purchases a 25% interest in Investee Z for $1,000,000 and has determined that the equity method of accounting is appropriate. At the acquisition date, the book value of Investee Z’s net assets is $3,000,000 and Company A’s proportionate share of those net assets is $750,000, resulting in a $250,000 difference when compared to the purchase price (or cost basis). Investee Z’s net assets as of January 1, 2020 are as follows:

Initial Measurement

After completing the fair value analysis, Company A determines that the fair value of Investee Z’s net assets is $3,700,000 based on the following:

- The fair value of cash, current assets, accounts payable, and other current liabilities all approximate their book values and no adjustments are necessary.

- The fair value of fixed assets is $3,000,000 and the remaining useful life is 20 years.

- Investee Z has certain unrecorded intangible assets of $200,000 with a definite life of 10 years.

Based on this analysis, the table below details the basis differences identified that make up the $250,000 difference between Company A’s cost basis of $1,000,000 and its 25% share of Investee Z’s recorded book value of $750,000.

Of Company A’s total $250,000 basis difference, $125,000 is directly attributable to the fair value step up for fixed assets and $50,000 is attributable to identified intangible assets that are not currently recorded on Investee Z’s books. The remaining $75,000 difference represents equity method goodwill.

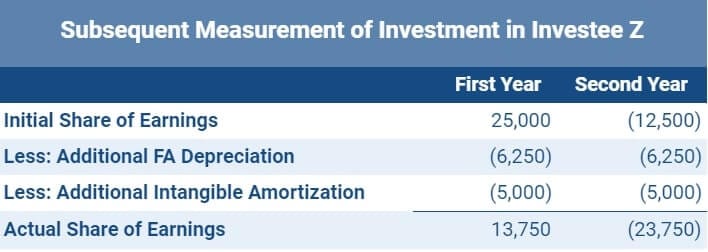

Due to these basis differences, each year Company A will adjust its proportionate share of Investee Z’s earnings to include an additional $6,250 of fixed asset depreciation ($125,000 basis difference / 20-year useful life) and $5,000 of intangible asset amortization ($50,000 basis difference / 10-year useful life) until both are fully depreciated/amortized. As equity method goodwill is not amortized, Company A will not make any adjustments for this amount.

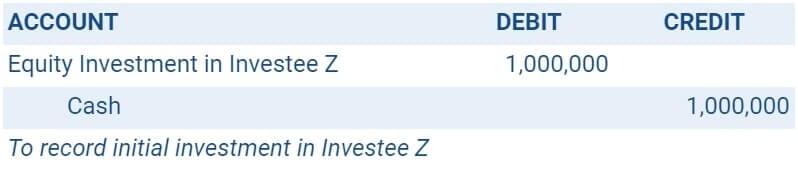

Although Company A has identified basis differences and equity method goodwill, it records its initial measurement of its equity method investment at cost basis with the following entry:

Company A does not record any impact from the identified basis differences or equity method goodwill upon acquisition. However, Company A will maintain a separate subledger for its investment in Investee Z in order to track these basis differences and the impact on equity earnings in future periods.

Subsequent Measurement

During the first and second years of Company A’s ownership, Investee Z has net income of $100,000 and a net loss of $50,000, respectively. To calculate its share of those earnings, Company A will first apply its ownership interest to the full year net income/loss and determine its initial proportionate share of earnings to be $25,000 income ($100,000 x 25%) for the first year and a $12,500 loss ($50,000x 25%) for the second year. Then Company A will factor in the basis differences it identified at the acquisition date in order to properly reflect the additional depreciation and amortization expense for the fixed asset fair value step-up and fair value of unrecorded definite lived intangibles. As a result, Company A determines its actual equity investment earnings for each year as follows.

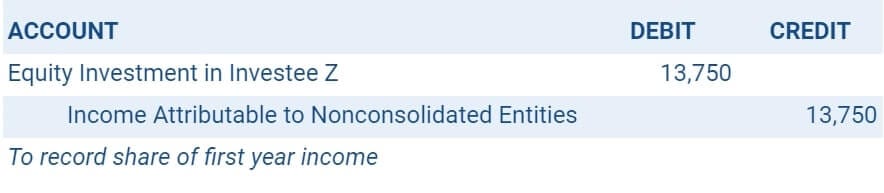

Company A will record the following entries:

If Company A had ignored the impacts of the basis differences identified at acquisition it would have recognized the incorrect amounts of income/loss each year and the equity method investment balance presented in its balance sheet would have been misstated. Therefore, Company A must ensure it is carefully tracking the basis differences and equity method accounting adjustments in its memo accounts. Both of the basis differences in this example have definite useful lives and so Company A will only apply the adjustments until the end of the applicable useful life. Incorrect tracking could result in continuing to adjust earnings for basis differences that have already been fully depreciated/amortized, resulting in inaccurate amounts presented in the consolidated financial statements.

Sale of equity method investment

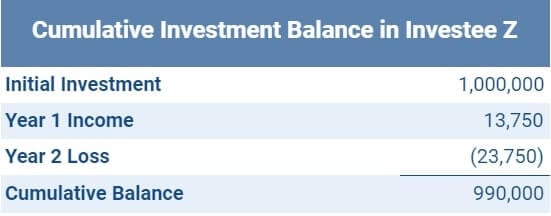

Assume that at the end of the second year Company A decides to sell its entire ownership interest in Investee Z to Company B for $1,000,000. Before the sale, Company A has a cumulative balance of its equity investment in Investee Z of $990,000 as follows:

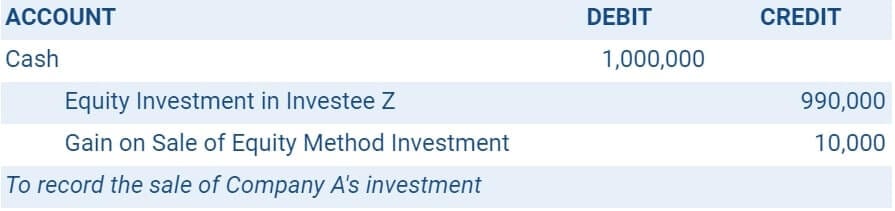

As a result of selling its ownership interest for $1,000,000, Company A will recognize a $10,000 gain on the sale and will record the following entry:

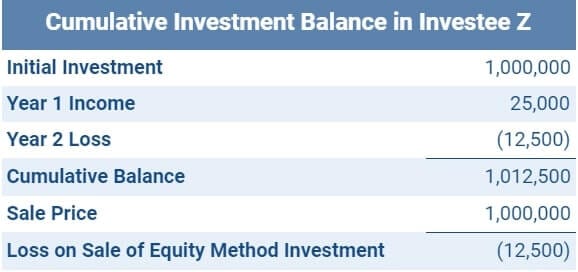

It is important to notice that if Company A had not properly tracked and accounted for equity method basis differences, the Company would have recorded the incorrect gain/loss on this sale. For example, if Company A had never accounted for basis differences while it held its ownership interest in Investee Z, it would have simply recorded its proportionate share of Investee Z’s earnings/losses each period with no adjustments. As such, the cumulative balance of its equity method investment in Investee Z as of the sale date would have been $1,012,500 and Company A would have incorrectly recognized a loss on the sale of $12,500 as shown below.

As this example illustrates, not properly tracking and accounting for equity method investments, including identifying and adjusting for basis differences, can directly impact a company’s financial results.

Summary

When applying the equity method of accounting, an entity is required to account for its investment under the same acquisition accounting and consolidation guidelines prescribed in ASC 805 even though its investment will be presented on a single line item in its balance sheet. Properly identifying the existence and amounts of basis differences between an investor’s cost basis and its proportionate share of an investee’s net assets is a critical step in applying the equity method of accounting. If basis differences are not correctly factored into equity method accounting, an investor risks misstating its earnings and balance sheet. Furthermore, an investor must carefully track basis differences throughout its ownership period to ensure appropriate accounting in each subsequent period as well as appropriate accounting should it later dispose of its investment.