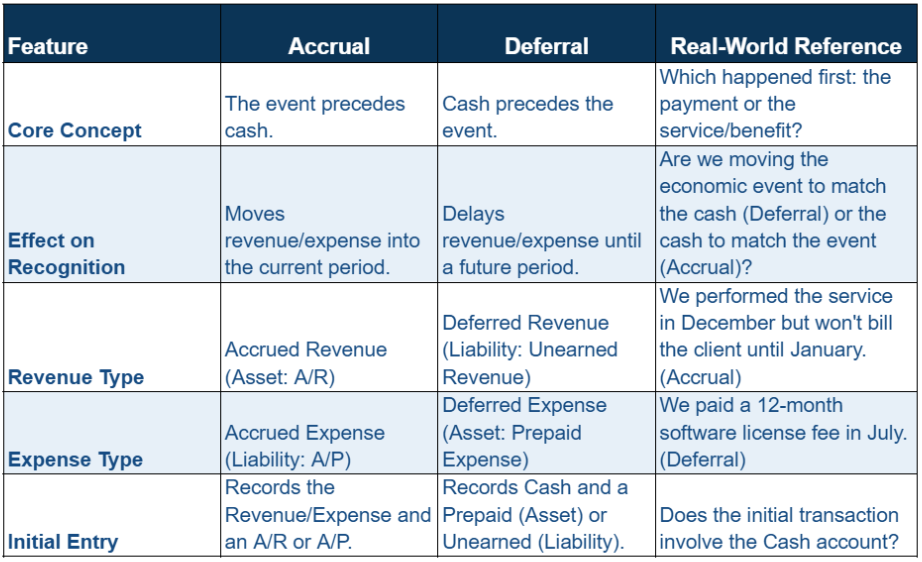

The vast majority of businesses operate on the accrual basis of accounting, which is mandated by the Financial Accounting Standards Board (FASB) for public companies. Why?

The accrual basis of accounting ensures the business recognizes revenue and expenses when they are earned and incurred, respectively, not just when money exchanges hands. Simply recognizing revenue when the business receives cash, also known as the cash basis of accounting, does not paint the full picture of the business’s standing. To sum up:

- Cash basis accounting: Tracks the money received or paid as it moves through the bank. This method can be misleading as it does not show the truth of the business. Common examples where this method fails would be a cash payment in December for a service you won’t deliver until January, or paying for insurance in July and being covered for a full year. Cash basis inherently distorts the full picture of this type of activity within the business.

- Accrual basis of accounting: Recognizes revenues and expenses when the underlying economic activity occurs. In the first example above, you would receive the cash in December but wait to recognize the revenue until you deliver the service in January.

- How accruals and deferrals fit in: Accruals and deferrals are the two types of adjusting entries that align economic activity with the proper reporting period in accrual-based accounting, making them essential for a true and fair view of financial performance. They are opposite sides of the same accounting coin.

Accrual and deferral defining factors

Accruals and deferrals are followed to ensure compliance with two core GAAP principles:

- Revenue recognition principle (ASC Topic 606): Revenue is recognized when a company satisfies its performance obligation by transferring promised goods or services to a customer.

- Matching principle: Expenses must be recorded in the same period as the revenues they helped generate.

What is an accrual?

- Core concept: The economic event happens before the cash exchange.

- The process: Accruals moves the recognition of a revenue or expense into the current period, even though the cash will move later.

- Two types:

- Accrued revenue: Revenue earned (service delivered) but cash not yet received (Asset: e.g., Accounts Receivable).

- Accrued expense: Expense incurred (benefit received) but cash not yet paid (Liability: e.g., Accrued Salaries Payable).

What is a deferral?

- Core concept: The cash exchange happens before the economic event.

- The process: Deferrals postpone or delay the recognition of a revenue or expense until a future period, even though the cash has moved now.

- Two types:

- Deferred revenue (unearned revenue): Cash received, but the revenue has not yet been earned (Liability: the company owes the good/service).

- Deferred expense (prepaid expense): Cash paid, but the expense has not yet been incurred/used (Asset: the company owns a future benefit, like prepaid insurance).

Similarities and differences: Accruals vs. deferral

- Both are required under the accrual basis of accounting (GAAP/FASB).

- Both are adjusting entries made at the end of an accounting period.

- Neither entry directly involves the cash account—they adjust a revenue/expense and a balance sheet account (Asset or Liability).

- Both ensure compliance with the revenue recognition and matching principles.