A deferred expense is a term you probably haven’t heard, but have likely seen in practice. Deferred expenses are categorized as a type of deferral, which is defined as, “the accounting process of recognizing a liability resulting from a current cash receipt or an asset resulting from a current cash payment with deferred recognition of related revenues, expenses, gains, or losses,” within FASB’s Conceptual Framework for Financial Reporting. You have likely encountered deferred expenses in practice, though you may have referred to them as prepaid expenses. In most cases these terms can be, and are very often, used interchangeably, representing an organizational preference.

What are deferred expenses?

To simplify FASB’s guidance, deferred expenses are instances where cash has been exchanged for goods or services but the benefits of those goods or services are going to be received in a future period. Some examples may include prepayments for software subscriptions and deferred insurance expense. These are two common examples where cash is often paid upfront for a service period extending beyond the initial cash exchange. As illustrated in the example below, to recognize this prepayment of deferred expenses, a journal entry is required to debit deferred software expense and credit cash for the full amount. Subsequent entries record the monthly expense and amortization by debiting the expense account and crediting the deferred expense account for the corresponding period. Let’s take a look at this below.

Deferred software expense example: Journal entry

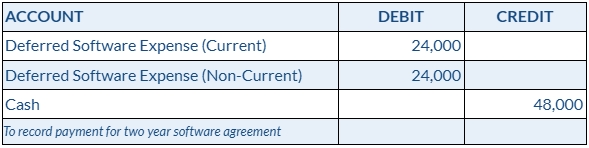

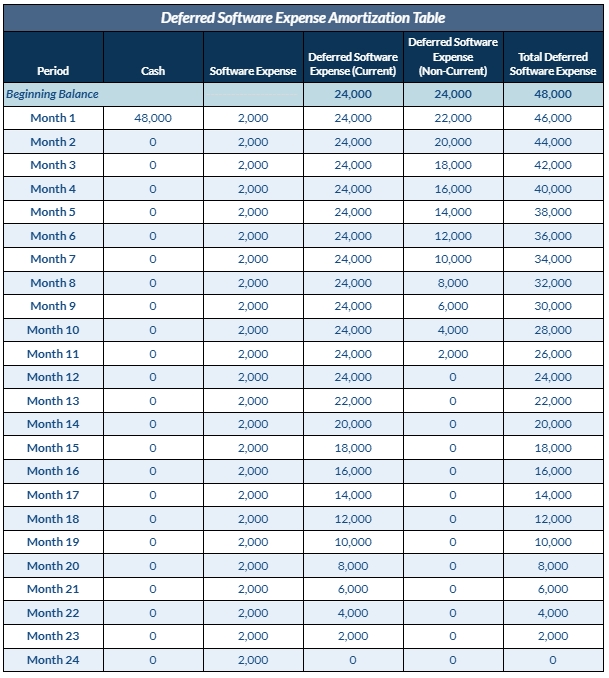

In our example, we have purchased accounting software in the amount of $48,000 for a period of two years. Payment was made in full for $48,000 on the start date of the policy. Let’s see how we initially record the deferred expense and subsequently record our expense and amortize the deferred expense account.

Journal entry 1

We first recognize our purchase of the software with the following entry. This entry also allocates the current portion (related to the next 12-month period) and the non-current portion (for the period beyond the next 12 months):

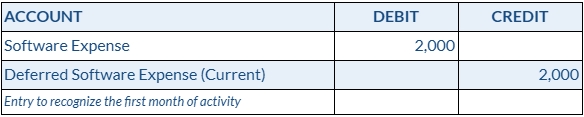

Journal entry 2

Now that we have recorded the payment of the software and recorded the corresponding deferred expense accounts, we can amortize the asset over the term of the policy. This entry is made monthly throughout the policy term.

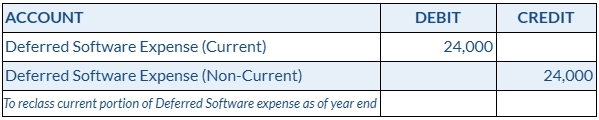

Journal entry 3

We will also need to make an entry at the end of our first year to properly reclassify the non-current portion of the deferred expense asset to the current asset account. This entry can be seen below:

Amortization schedule

For a complete view of how these entries come together, an amortization schedule is shown below outlining how the deferred expense balance is reduced, or amortized, throughout the term of the policy.

Summary

At this point, you should now understand what a deferred expense is and the full accounting cycle involved. This same process can be applied to various deferred expenses within an organization to prepare accurate and compliant financial statements.

Another common example of accrual basis accounting coming into play are accrued expenses. If you are interested in learning how to account for your accrued expenses, check out our helpful blog, “Accrued Expenses and Liabilities: Definition, Journal Entries, Examples, and More Explained.”