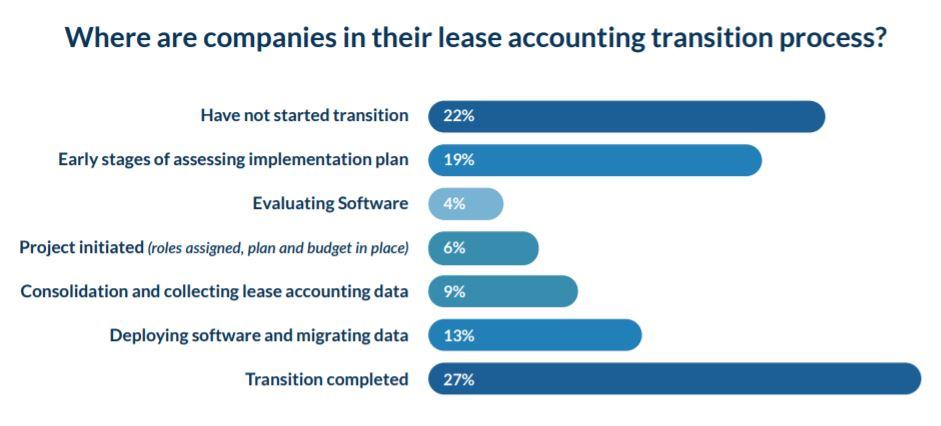

Nearly 40% of private companies surveyed are still in the very early stages of assessing their ASC 842 implementation plan

ATLANTA – Dec. 13, 2021 — With the final ASC 842 lease accounting compliance deadline finally in sight, private companies are quickly shifting focus after 73% deprioritized their lease accounting transition in 2020, according to a new report, To the ASC 842 Finish Line and Beyond: A Survey of How Private Companies Are Preparing for the Lease Accounting Transition, from accounting technology provider, LeaseQuery.

In a survey of more than 270 accounting and finance professionals, LeaseQuery asked accountants – many of whom are still in the beginning stages of their company transition journey – to share their biggest priorities and roadblocks as the FASB ASC 842 lease accounting deadline approaches.

The gap between private companies that believe they are on track to comply with ASC 842 and meet the tight transition deadline and those who have actually begun the process is surprising, especially given the firsthand experiences shared by public companies.

Private companies predict a challenging road ahead as they prepare for adoption in correlation with new significant changes to the face of financials over the last year. LeaseQuery’s survey uncovered companies’ top three concerns that may impact lease accounting compliance:

- COVID-19 pandemic lease modifications: As the business case for health and safety above all else is clear in a post-pandemic environment, 73% of companies said their lease accounting transition was deprioritized, or that resources were deployed to other priorities during the pandemic.

- Staffing and talent challenges: From the Great Resignation to employee burnout, talent acquisition and retention is a major pain point for companies currently, with 25% reporting having to deploy staffing resources to other priorities forcing them to reimagine, redesign and redeploy their lease accounting processes.

- Going it alone: While deciding to add new team members to complete the ASC 842 transition comes down to the way companies use technology or lease accounting partners, 26% of companies have either added to their lease accounting transition team or are actively searching for the right fit.

“The ASC 842 lease accounting transition will likely affect more areas of the business than some may expect,” said Jennifer Booth, LeaseQuery’s Accounting Vice President. “Although achieving compliance should be businesses’ number one lease accounting priority, it’s also time to start shifting focus to assess what’s next after their transition. Implementing technology now allows teams to focus on higher priorities and opens businesses up to key insights that will help plan for and protect their future.”

For more information, read the full report: To the ASC 842 Finish Line and Beyond: A Survey of How Private Companies are Preparing for the Lease Accounting Transition.

About LeaseQuery

LeaseQuery makes accountants’ lives easier by simplifying the complex with technology. More than 25,000 financial professionals globally rely on our cloud-based, CPA-approved solutions and in-house accounting expertise to comply with confidence across various FASB, GASB and IASB accounting standards. Our software helps businesses minimize risk, increase efficiency and reduce costs. Learn more about LeaseQuery’s core lease accounting solution, which focuses on easing the mandatory transition to ASC 842, IFRS 16, GASB 87 and GASB 96, or explore additional accounting tools. For more information, visit LeaseQuery.com.

Additional Resources

- Learn more about LeaseQuery

- Follow LeaseQuery on LinkedIn and Twitter

- Read LeaseQuery’s blog articles