1. Disclosure requirements for lessees under IFRS 16

2. Using software to generate accurate and efficient disclosures

3. Quantitative disclosures for lessees

- Amounts recognized on the income statement

- Maturity analysis of lease liabilities

- Information about ROU assets

- Cash flow and other additional entity specific information

4. Summary

IFRS 16 Leases is a change from previous guidance due to its single-model approach for lessees whereby all lessee leases post-adoption are recognized as finance leases and capitalized. Unlike IAS 17, where the distinction between capital leases and operating leases requires only capital leases to be recognized on the balance sheet, IFRS 16 provides greater transparency to an organization’s obligations. In conjunction with the change of accounting treatment, the new guidance also includes expanded disclosure requirements for all lessees.

Disclosure requirements for lessees under IFRS 16

In this article, we’ll provide an overview of the disclosure requirements for lessees and also discuss the supporting data necessary for preparation of your company’s annual disclosures. The disclosure requirements include both qualitative and quantitative elements, specifically:

- Discussion of leasing activities

- Descriptions of significant judgements and accounting policy elections applicable to the lease population

- Information about the amounts recognized in the financial statements related to an organization’s leasing activities

Below is a discussion on the expanded quantitative disclosures.

Using software to generate accurate and efficient disclosures

Without assistance from a software solution, accumulating the data for the quantitative lease disclosures can be a time-consuming task. After compiling the necessary information and performing the required calculations, the company then validates the accuracy of the calculations for its internal controls and audit requirements. Additionally, calculations will need to be updated on an ongoing basis for any modifications, lease additions, or terminations during each reporting period.

LeaseQuery’s reporting studio includes an IFRS 16 Complete Disclosures Report that can be generated for the organization’s entire lease portfolio. This report allows a company to quickly aggregate the data necessary to complete its lease footnote in accordance with IFRS 16. The guidance recommends quantitative disclosures be presented in a table (IFRS 16 para. 54). However, an organization has the option to deviate from this presentation if a more appropriate format exists. In keeping with the guidance, LeaseQuery has established its reporting in a tabular format.

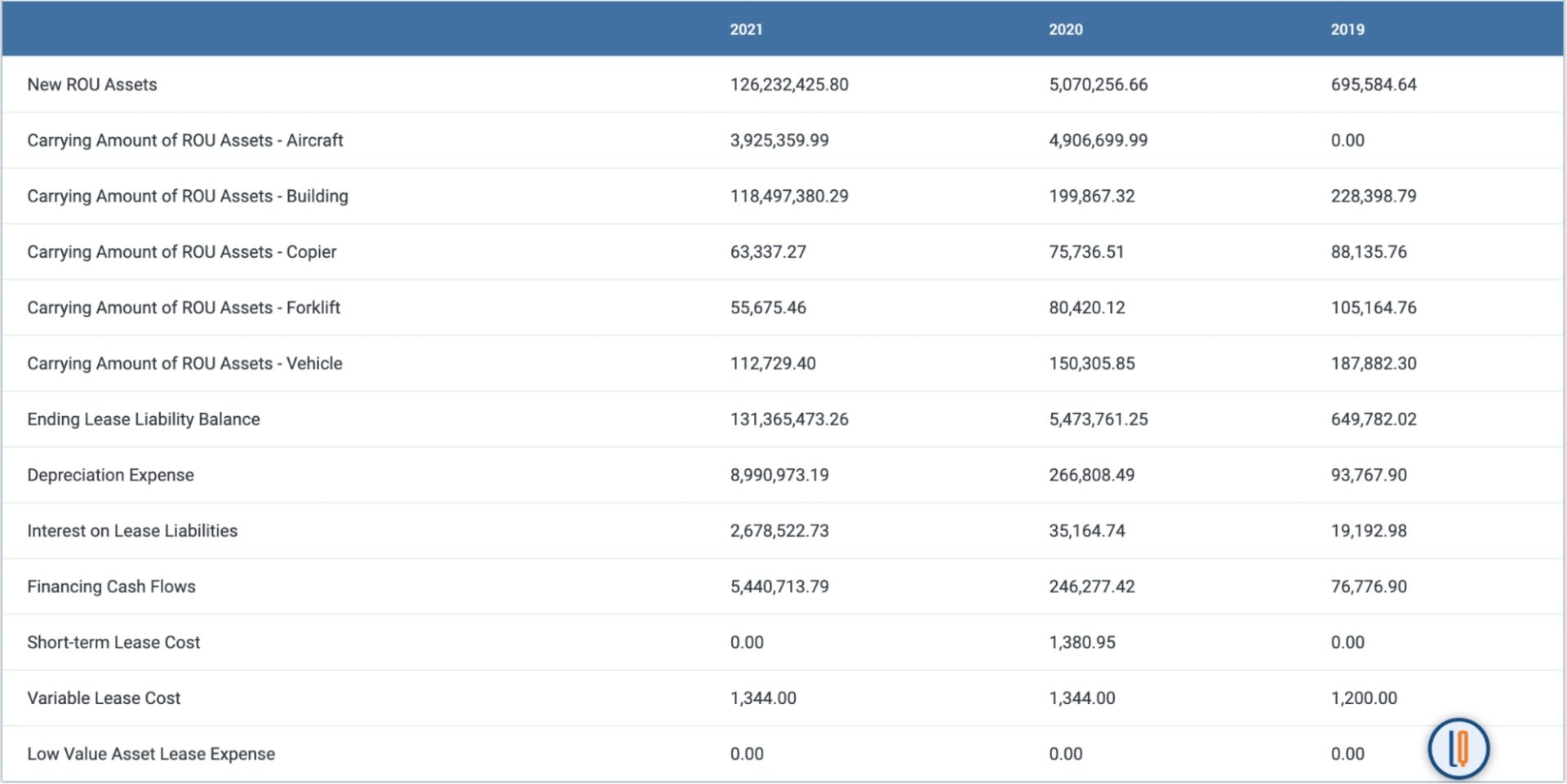

The screenshot below showcases the quantitative disclosures required under IFRS 16 and their summary presentation in LeaseQuery. The full report can be exported to Excel, allowing users to quickly copy and paste the quantitative data into the footnotes. Additionally, the Excel export allows users to analyze the details of each balance by lease.

LeaseQuery’s Complete Disclosure Report for notes to the financial statements:

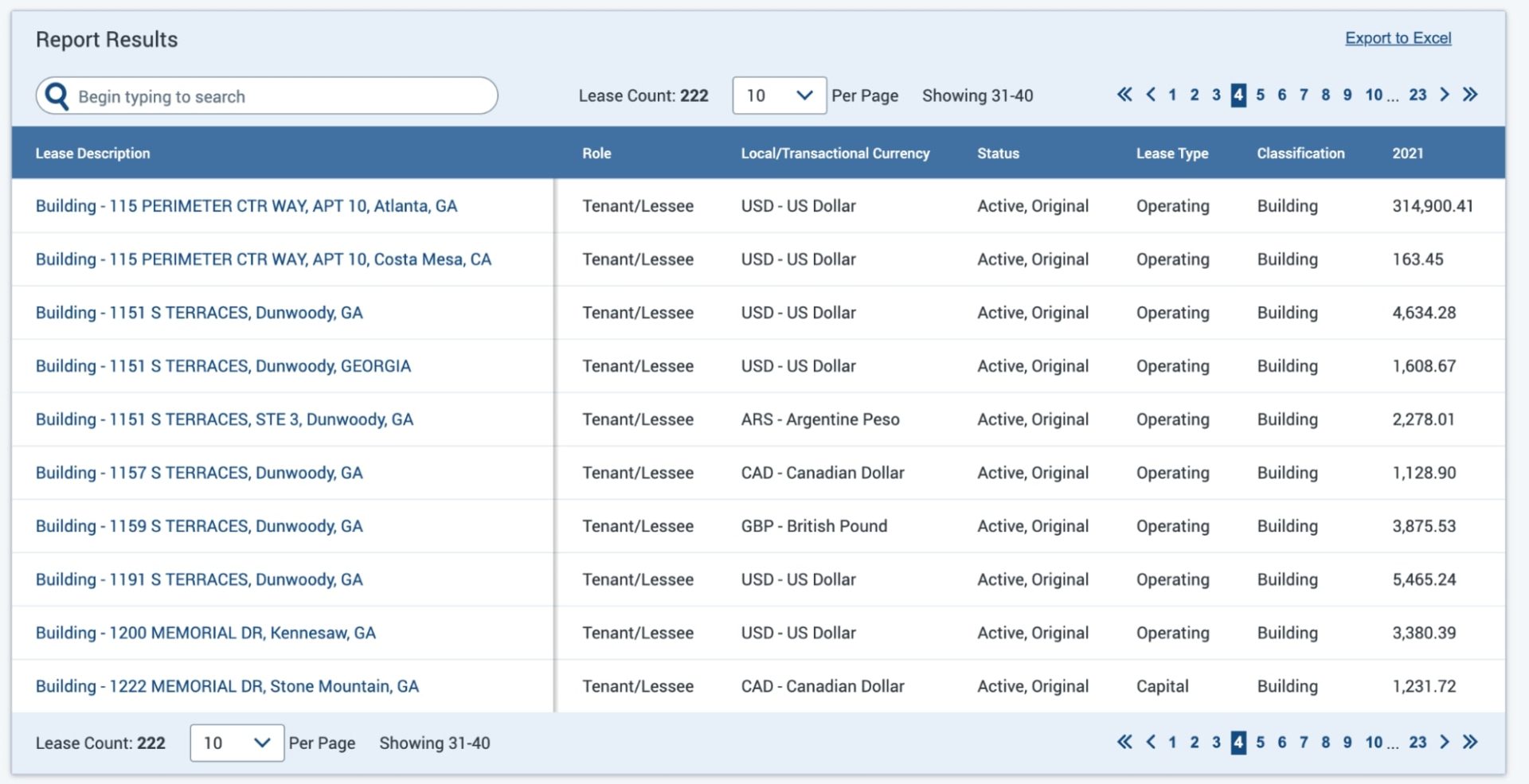

As noted above, in addition to the summarized company-level information, LeaseQuery software provides the ability to drill down to the individual leases within each disclosure calculation. For example, summary information at any level of an entity’s organization (i.e. business unit, department, or region) can be retrieved, along with the individual lease data.

An excerpt of LeaseQuery’s Drilldown Report of the individual lease detail related to the footnote disclosure for financing cash flows:

Quantitative disclosures for lessees

The quantitative disclosures required under IFRS 16 are grouped into four buckets:

- Amounts recognized on the income statement

- Maturity analysis of lease liabilities

- Information about ROU assets

- Cash flow and other additional entity specific information

Amounts recognized on the income statement

The quantitative disclosures related to lease expenses provide additional information on the nature of these expenses. The disclosure of expenses stemming from the following are required under IFRS 16:

- The ROU asset and lease liability on the balance sheet, such as depreciation and interest expense

- Out-of-scope leases as a result of the election of practical expedients, such as short-term leases and leases of low value assets

- Variable consideration within leases not included in the measurement of the lease liability due to the nature of the payments

If a company enters into any sub-lease arrangements, the income on these arrangements should also be disclosed.

LeaseQuery’s Complete Disclosure Report excerpt related to lease cost:

Maturity analysis of lease liabilities

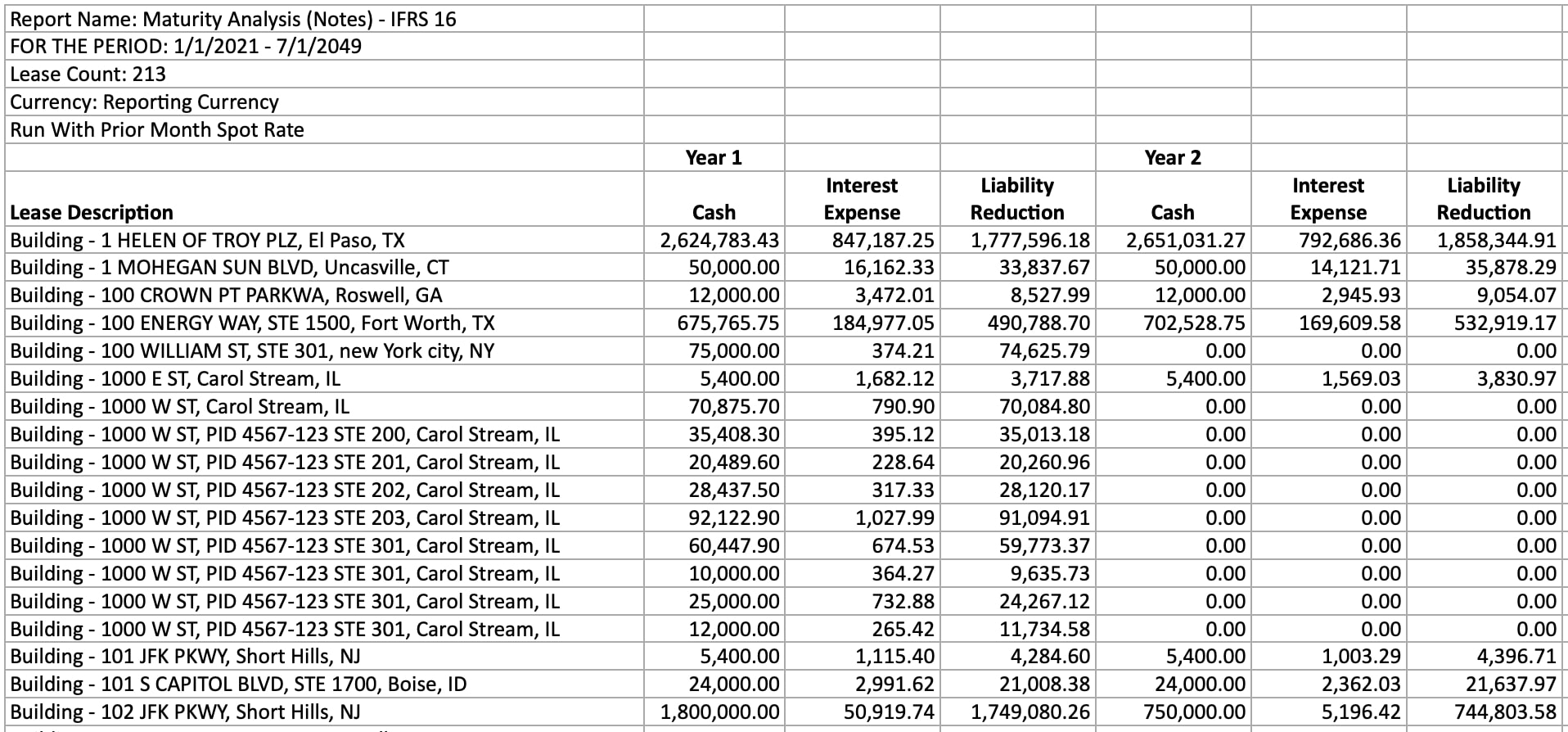

The maturity analysis reconciles the undiscounted expected future cash flows to the lease liabilities recorded on the balance sheet. As required by IFRS 16, LeaseQuery’s standard report presents the maturity analysis on an annual basis for the first five years and all remaining years after in increments of five years for all in-scope leases. LeaseQuery creates the maturity analysis table from all of the lease data that has been provided to facilitate this disclosure and users are able to see the data at a summary level or at the lease level.

LeaseQuery’s excerpt of a maturity analysis:

Information about ROU assets

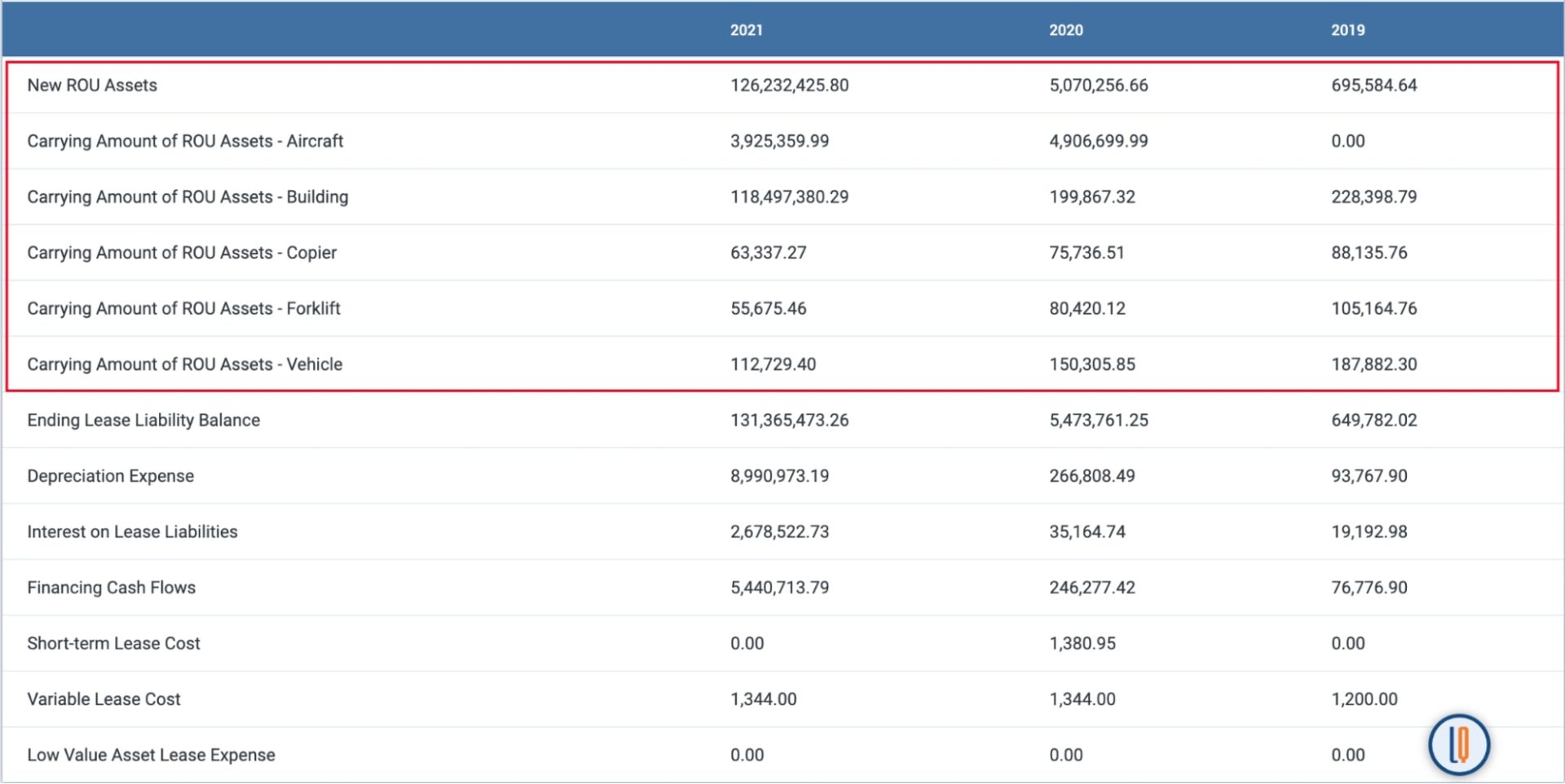

With respect to the quantitative disclosures pertaining to ROU assets under IFRS 16, a lessee is required to disclose:

- ROU asset additions during the reporting period, from both new leases and lease modifications

- The carrying value of ROU assets by asset class as of the end of the reporting period

An excerpt from LeaseQuery’s Complete Disclosure Report for the ROU asset disclosures:

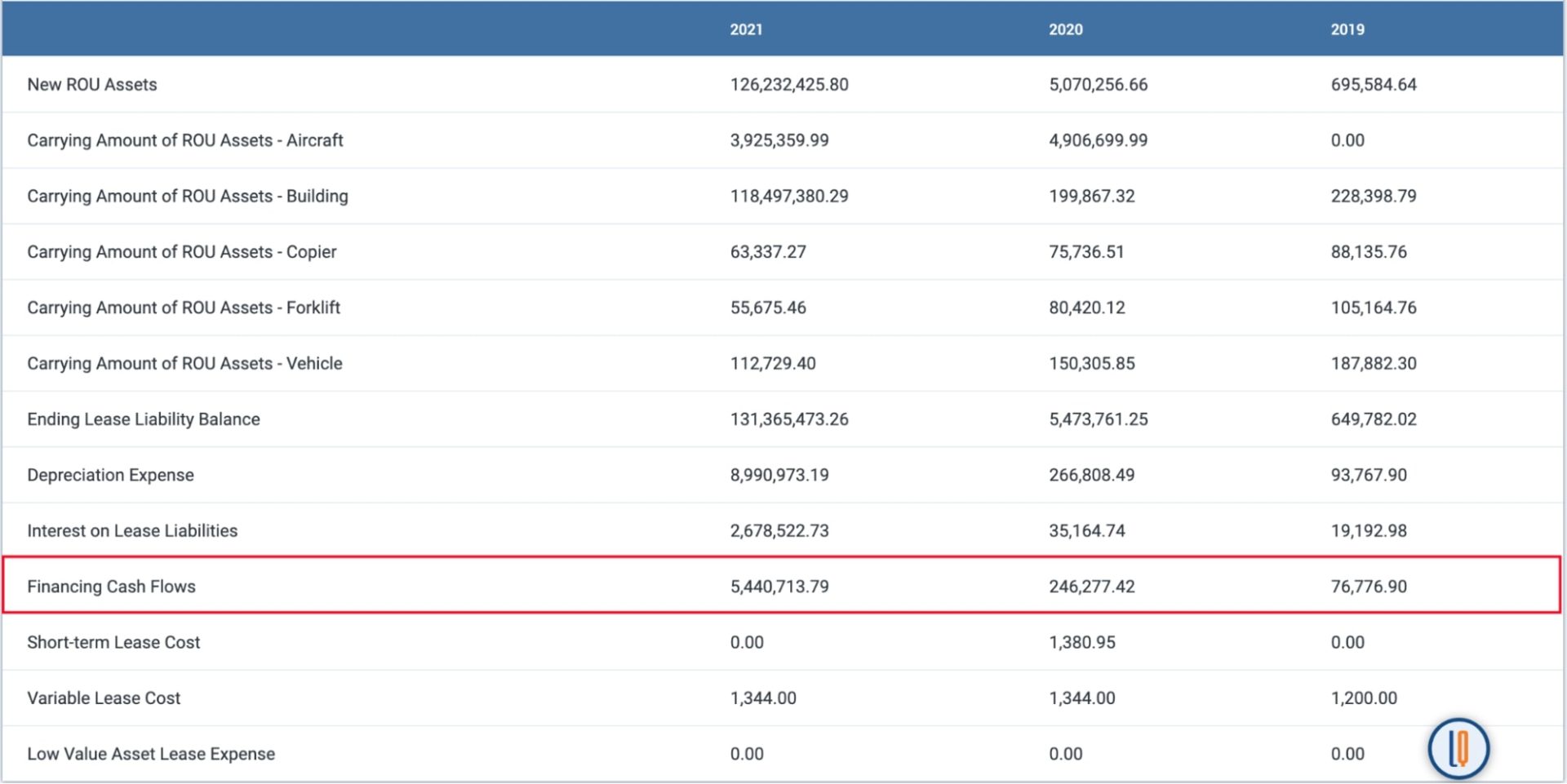

Cash flow and other additional entity specific information

Other quantitative disclosures required by IFRS 16 include but are not limited to:

- Total cash outflows from leases for the reporting period

- Potential future cash flows not captured in the computation of the lease liabilities, related to items such as variable lease payments, leases not yet commenced, extension and termination options, and residual value guarantees

- Gains or losses from any sale-leaseback transactions

Supplemental information such as the nature of leasing activities and potential exposures from these activities are included to facilitate a stakeholder’s understanding of the cash flows and operations of the entity.

LeaseQuery’s Complete Disclosure Report excerpt of cash flow and other additional entity specific information:

Summary

Using software purpose-built to comply with IFRS 16 to prepare a company’s lease disclosures will save accounting teams time and ensure the accuracy of the disclosures. This will allow the company to focus its efforts on the qualitative requirements of the disclosure: descriptions of its leases, features of lease arrangements such as variable lease payments and residual value guarantees, and its accounting policies with regards to discount rates, lease and non-lease components, and short-term leases.