Lease Liabilities Index Report

AN ANALYSIS OF MORE THAN 400 COMPANIES' BALANCE SHEETS DOWNLOAD THE PDFBalance sheet liabilities skyrocket in lease accounting transition

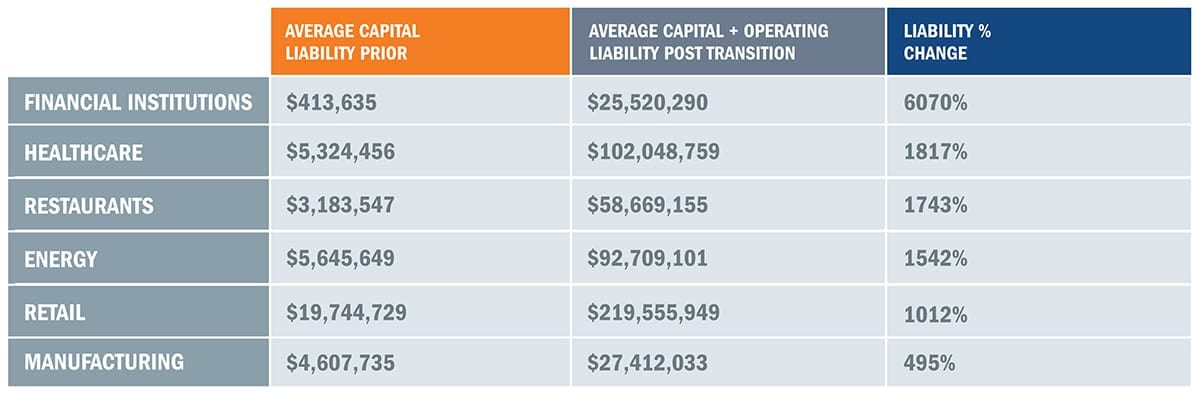

The analysis found that the implementation of the new lease accounting standard led to average balance sheet lease liabilities increases of

When the FASB’s changes to lease accounting standards were released in 2016, it was hailed as one of the biggest changes to accounting in decades. After implementation of the new rules began in earnest in 2019, one thing became clear: it’s also one of the biggest changes to balance sheets in decades.

According to LeaseQuery’s Lease Liabilities Index, an analysis of more than 400 companies’ balance sheets pre- and post-transition, companies who have not yet transitioned need to be preparing for an overhaul of their financial snapshot.

How ASC 842 disrupted

the balance sheet

Under the old lease accounting standard, operating leases were considered off-balance-sheet transactions. The expense associated with the arrangements was recognized in the income statement, but there was not any balance sheet impact. This made it difficult to understand the volume of a company’s commitments.

To increase transparency, the FASB issued ASC 842, the new standard for lease accounting. For operating leases specifically, ASC 842 requires recognition of a right of use (ROU) asset and a corresponding lease liability upon lease commencement.

INDUSTRY SPOTLIGHTS

While every company and industry has a unique leasing strategy and lease portfolio to contend with, the new standard is of particular importance to sectors with a high volume of leases. The Lease Liabilities Index analyzes lease accounting transition impact across numerous industries. In this report, we highlight six critical industries.

FINANCIAL INSTITUTIONS

The financial industry is no stranger to scrutiny. Analysts, economists and investors alike watch it closely as a bellwether of the economy and how the flow of capital is faring.

While lease accounting won’t change how financial institutions make loan or leasing decisions, it is already having a huge impact on how those decisions appear on balance sheets. As banks recognize operating leases for retail branches and office space, their capital ratios could be modestly reduced. Still, the underlying fundamentals of the industry remain unchanged, making communications with key stakeholders critical to ensure stability.

The banking industry specifically has contended with changing regulations for years. With lease accounting implementation coming right before companies will need to be compliant with the new deadline for CECL (Current Expected Credit Loss), accounting compliance will continue to be a significant challenge for the industry over the next several years.

+6070%

+1817%

HEALTHCARE

Whether public or private, hospitals and healthcare organizations both lease a wide range of critical resources that aid in care. From facilities to medical equipment and technology, the industry is highly impacted by the lease accounting rule change.

But healthcare organizations face a unique challenge in preparations — their focus on care is always top priority. Healthcare financial departments may be responsible for lease accounting implementation efforts, but have competing priorities that may more directly tie back to improved care.

Even as the industry responds to regulatory upheaval, change, and an increased focus on high-quality care, it’s critical to avoid overlooking this key accounting change that can impact leasing strategy, terms with lenders and more.

RESTAURANTS

In the restaurant industry, large public companies, franchisors, and smaller owner/operators with a few concepts have one thing in common: numerous leases. In addition to the physical storefront, restaurateurs often lease out key pieces of equipment—from kitchen appliances to beverage fountains and taps.

With all of those lease arrangements moving to the balance sheet, in an industry deeply challenged by rising labor and commodity costs, restaurants have a major challenge ahead. The rule change may be a prompt for operators to reconsider lease vs. buy decisions.

The industry also continues to be a popular target for private equity investors and M&A, meaning that restaurant business leaders should take the time to not only understand the accounting impact of the new standard, but also the questions it will raise around EBITDA and valuation. Communication with investors, lenders, and other key stakeholders will be critical.

+1743%

+1542%

ENERGY

Sourcing, refining, and delivering energy to users—whether through oil and gas or utilities—is capital intensive work. Land, building, equipment, and drilling contracts will need to be assessed to see how the new standard applies.

Land easements, foreign currencies, and take-or-pay provisions can further complicate an already complex process in the energy industry overall. Furthermore, the power and utilities sector will see major impacts in light of the new standards, as the determining factor to recognize leases now requires the party to control the use of the underlying asset to conclude as to whether a contract represents a lease.

These compliance challenges come as the industry contends with volatility abroad, the push toward renewables, and digitization-all of which are changing demand and decision making. As a result of the new guidance, utility companies, for example, must re-evaluate the change in lease definition, in addition to calculating the amounts to be recognized on the balance sheet for the contracts that were determined leases. In addition, as energy industry businesses alter their long-term strategy for a greener world, lease arrangements are likely to be in focus.

RETAIL

The retail industry has seen a significant impact from the new lease accounting rules. Many of the biggest brands rely on leases as a part of their operating model, and the initial transition has brought greater transparency to their real estate and capital strategy.

The rule change arrives at the same time as retailers are contending with other significant headwinds — from industry bankruptcies and changing consumer preferences to tax changes and tariffs that could further challenge margins.

Looking ahead, 2020 will be another critical year for retailers in the transition process as they seek to optimize their leasing and location strategy in collaboration with growing digital demands.

+1012

%

+495%

MANUFACTURING

Every twist and turn of the supply chain — from concept to fulfillment — presents potential for lease exposures. Manufacturers are both lessors and heavy users of leases in order to meet the needs of their global supply chains.

Manufacturers should look at lease accounting not as another compliance burden, but as an opportunity for further efficiency and streamlined processes. The industry is in the midst of a technology evolution, leveraging Internet of Things (IoT) and other connected solutions to improve output and reduce redundancy.

Through better insight into their total lease liability, manufacturers can ensure contracts are optimized and leases are managed effectively. Arming the finance department with the tools to quickly find out where assets are and if they are in use ultimately improves the utilization and tracking of assets. As technology changes the type of equipment used in key processes, manufacturers should take those prompts to consider their lease terms and arrangements.

Championing & Communicating Change

Change is often forced, but that doesn’t mean that compliance can’t bring positive outcomes.

The intended goal of changes to lease accounting is increased transparency. In these transition years, that transparency is going to mean a lot of questions. Stakeholders will see increasing liabilities and need to understand why, and it’s the role of the finance department — with support of the organization — to communicate clearly the impact of the rule change to financial health and the underlying fundamentals and financials health of the organization.

Companies might also benefit from sharing key takeaways or benefits that came with implementation — for example, identifying existing suboptimal lease contracts or reassessing lease vs. buy decisions.

Transitions are never easy, but by championing change and being a vocal guide to the impact and deeper business insight, companies will be better positioned to ease any stakeholder concerns.

YOUR TRANSITION JOURNEY

For private companies and nonprofits, the level of balance sheet change ahead, as well as lessons learned from those who have already adopted should be a major wake-up call.

37%

of companies in early stages anticipate a difficult transition

67%

of companies in later stages have experienced difficulty

Communicating these significant changes to stakeholders — including internal leadership teams, board members, and investors — must also be considered as a part of your transition plan.

ABOUT LEASEQUERY

LeaseQuery helps more than 10,000 accountants and other finance professionals eliminate lease accounting errors through its CPA-approved lease accounting software. It is the first lease accounting software built by accountants for accountants. By providing specialized consulting services in addition to its software solution, LeaseQuery facilitates compliance with the most comprehensive regulatory reform in 40 years for companies across all sectors.

ABOUT THE LEASE LIABILITIES INDEX

LeaseQuery’s Lease Liabilities Index is a regular analysis of more than 400 public, private, and nonprofit organizations’ financials as they implement new lease accounting standards. The index is designed as a benchmarking resource to help companies assess and communicate changes to their stakeholders.

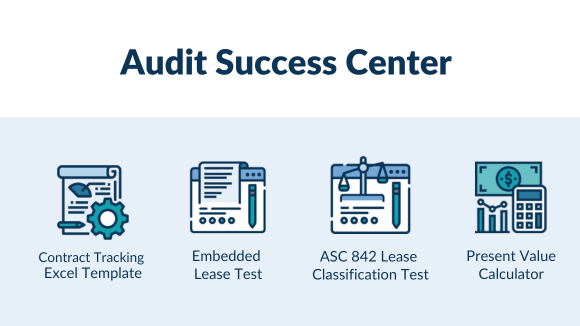

Like this report? Check out some of our free tools.

Free Lease Accounting Software

Comply with confidence for up to nine leases under ASC 842 & IFRS 16.

GASB Lease Accounting RFP

Use our GASB specific RFP to start evaluating software vendors today.

Lease Accounting Software RFP

Use our RFP to start evaluating lease accounting software vendors today.

Lease vs Buy Calculator

Perform a break even analysis with our free Lease vs Buy excel template.

GASB Lease Tracking Template

Use this free tool to create an inventory of your leases.

Embedded Lease Test

Use this free tool to determine if your contract contains a lease.

Lease Asset Tracker

Use this free tool to easily document your leases.

Capital vs. Operating Lease Test

Use this free tool to determine your lease classification.

Present Value Calculator

Use this free tool to calculate the present value of your minimum lease payments.