What is depreciation?

Depreciation is an accounting method used to spread out the cost of an asset over its useful life to reflect its reduction in value from wear and tear or obsolescence. Depreciation generally applies to a company’s fixed assets or to its leased right-of-use assets from finance leases.

Depreciation expense

Depreciation expense is an income statement item recognized throughout the life of the asset as a “non-cash” expense. While depreciation methods vary, the total amount of depreciation recorded throughout the life of an asset remains constant; it is the timing of the expense that changes.

Accumulated depreciation

Accumulated depreciation is a contra asset account that is the associated balance sheet line item for depreciation. At the same time that depreciation expense is recorded as a debit, accumulated depreciation is recorded as a credit. This contra asset account represents the reduction of the asset’s value over time and has a normal credit balance.

Accumulated depreciation offsets a fixed asset’s balance. As such, an asset’s net book value (NBV) at any particular point in time is its historical cost minus its accumulated depreciation balance.

Accumulated depreciation remains on the balance sheet until the asset is disposed of. At disposal, the accumulated depreciation is debited to clear it off the books.

Depreciation methods in accounting

Under US GAAP, there are four methods of calculating depreciation organizations can use:

- Straight-line depreciation method

- Declining balance depreciation method

- Units of production depreciation method

- Sum-of-the-years’ digits depreciation method

This article discusses the sum-of-the-years’ digits depreciation method.

Sum-of-the-years’ digits depreciation

The sum-of-the-years’ digits depreciation method (SYD) is calculated by adding up all the digits in the asset’s useful life, in years, and using that sum to calculate a percentage of the remaining life of the asset. That percentage is then applied to the depreciable base (asset cost minus the salvage value, if applicable) to calculate depreciation expense for the period. This ultimately accelerates depreciation, and front-loads the depreciation expense in earlier years and less as time goes on.

As a quick example, for an asset with a 5-year useful life, the sum of the useful life’s years’ digits would be 5 + 4 + 3 + 2 + 1 = 15. The annual depreciation expense for Year 1 would be one third (5/15) of the asset’s value. In Year 2, the annual depreciation expense percentage would be approximately 27% (4/15). Then, in Year 3 the percentage would be one fifth (⅕ = 3/15).

Alternatively, instead of manually adding the digits together, you can use the following formula for the sum-of-the-years’ digits denominator:

SYD:

where n is the useful life of the asset.

Using this formula in our example above, we would have 5(5+1)/2, or 15, and ultimately get to the same result.

We will use this SYD in our full example below.

Example: Sum-of-the-years’ digits depreciation

For example, assume we are a manufacturing organization that buys a specialized milling machine, using the below facts:

- Purchase Cost: $550,000

- Estimated Salvage Value: $50,000

- Estimated Useful Life of the Asset: 5 Years

- Depreciable Base: $500,000 ($550,000-$50,000)

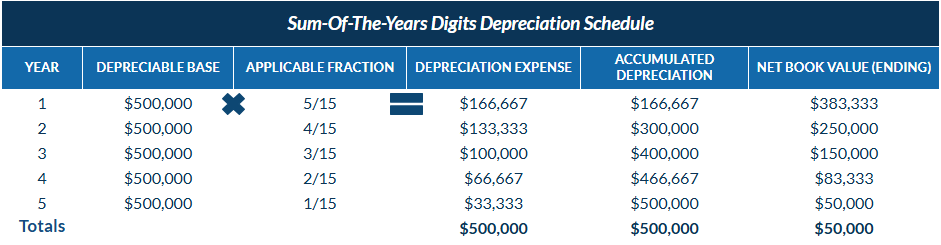

Step 1: Calculate the sum-of-the-years’ digits

The useful life is 5 years, so to calculate the denominator in our equation, sum up 5 + 4 + 3 + 2 + 1 = 15. Alternatively, using the formula above, n(n+1)/2, where n is the useful life in years, we get to 15 as the sum-of-the-years’ digits.

Step 2: Create the depreciation schedule

Input the depreciable base, followed by the applicable fraction in their respective columns. To calculate the depreciation expense, multiply the depreciable base by the applicable fraction to calculate that year’s total. For example, the first year’s annual depreciation journal entry would be recorded as follows:

At the end of Year 1, total depreciation expense and accumulated depreciation are $166,667. The net book value is calculated by taking the cost ($550,000) minus the accumulated depreciation ($166,667). The book value doesn’t drop below its salvage value, even at the end of its useful life; the asset is depreciated down to its residual amount.

At the end of Year 2, the same calculation is performed, multiplying the depreciable base by the applicable fraction (4/15) to get to the depreciation expense of $133,333. The entry is below:

Each year, a similar entry is made to recognize depreciation expense and add to the accumulated depreciation balance.

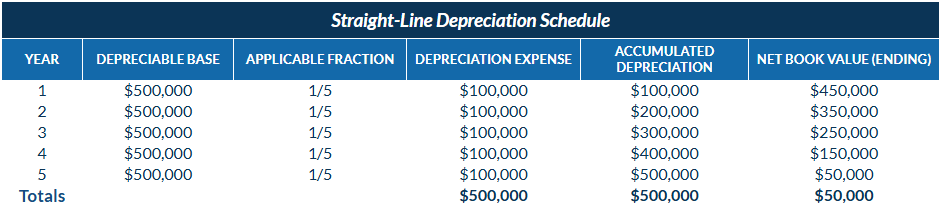

If we had used a different method of depreciation (for example, the straight-line depreciation method), the schedule would look like this:

As you can see, the total amount of depreciation is identical no matter which depreciation method is used. The timing of the expense recognition is all that changes.

Sum-of-the-years’ digits depreciation method: When does it make sense?

The sum-of-the-years’ digits method makes the most sense to apply when an asset’s economic utility is heavily front-loaded. This can happen if the asset is subject to:

- Rapid Obsolescence: The asset loses value quickly due to technological advancements rather than physical wear, or

- Diminishing Efficiency: The asset requires significantly higher maintenance costs in later years to maintain the same level of output as in earlier years.

As such, this depreciation method is most appropriate for assets that are more efficient when new, as it aligns the highest depreciation costs with the period of greatest productivity. Asset types include:

- Vehicles: Automobiles and delivery trucks typically incur the highest mileage and utility in their first years. As they age, maintenance and repair costs rise disproportionately, making the sum-of-the-years’ digits method an ideal depreciation method to smooth the total cost of ownership over the asset’s useful life.

- Technology/Hardware: Servers, data center equipment, and high-performance workstations typically provide their peak competitive advantage immediately upon purchase and become technologically inferior long before they physically fail.

- Manufacturing Equipment: Specialized heavy machinery often operates at peak speed and precision when new, but requires frequent calibration and part replacement as it ages. The sum-of-the-years’ digits method aligns depreciation expenses with the asset’s most productive years.

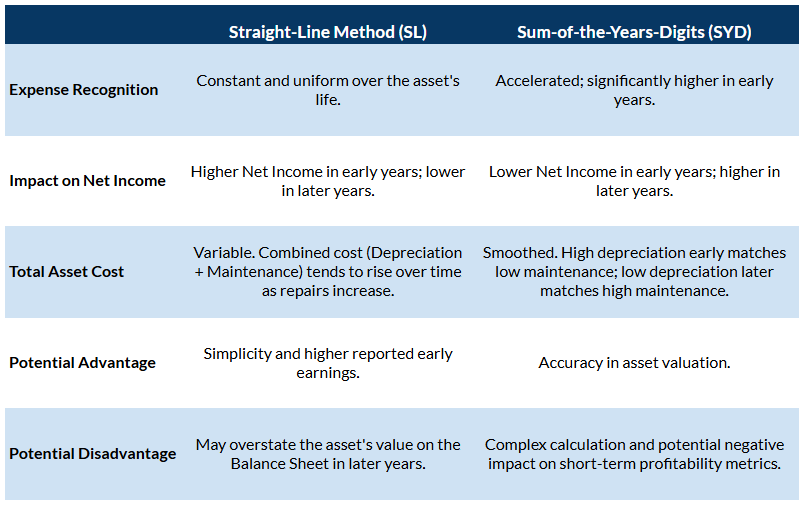

Below summarizes a few key differences between the straight-line method and the sum-of-the-years’ digits method of depreciation:

Summary

The sum-of-the-years’ digits method of depreciation is ideal for assets that experience rapid economic obsolescence or high initial utility. While more complex to administer than the straight-line method, SYD offers a more accurate reflection of how specific assets are consumed, ensuring financial statements present a true and fair view of an entity’s position.