In order to comply with the revised requirements for lease accounting under FRS 102, particularly those outlined in Section 20, you’ll need to conduct a thorough lease inventory. This will require you to gather, review, and consolidate your lease information. Though it will require careful planning and cross-departmental collaboration, the right approach will save you time and effort in collecting the right data. Here’s how to get started.

1. Scope your leases

Your first instinct may be to compile all of your possible leases together into an Excel sheet. However, if some of your leases are immaterial, short-term in nature, or otherwise don’t meet the definition of a lease, this approach may waste time and resources. Instead, consider the following definition of a lease and the scoping exemptions from the new lease accounting standard before finalizing your lease listing.

Defining a lease under FRS 102

Under the updated FRS 102, a lease is defined as an agreement that conveys the right to control the use of an identified asset for a specified period in exchange for consideration (usually payment). Central to this definition is the concept of control. The lessee must both:

- Obtain substantially all of the economic benefits derived from the asset.

- Have the ability to direct its use during the lease term.

When compiling your lease portfolio, ensure you also evaluate your non-lease contracts for any embedded leases that might fall within this definition.

Exemptions

Not every lease will need to be captured in the inventory. Consider the following exemptions when scoping your lease portfolio:

- Short-Term Leases: Exemptions exist for leases with a duration less than or equal to 12 months, without a purchase option. If you have leases that qualify for this exemption, ensure that you segregate these leases for separate disclosure, even if they are not capitalised.

- Materiality Thresholds: FRS 102 does not set a threshold for materiality, but includes exemptions for low-value assets. Establish and record practical criteria to omit low-value leases. Often, low-dollar items such as office equipment or small-scale technology leases can be excluded based on a predetermined capitalisation limit. When applying this threshold, consider not just the asset value but the corresponding lease liability.

Document your rationale for any thresholds or exclusions—this will be important during discussions with auditors or when reviewing your disclosures.

2. Find your leases

Review internal processes

To build your lease inventory, you will need to understand your organization’s current processes so you can identify the departments to engage. Begin by mapping your organization’s requisition process. Understand how lease-related agreements are initiated and which departments have the oversight on these contracts. Departments such as real estate, procurement, and facilities typically house much of this information. Additionally, your internal audit team may have already compiled process maps or walk-throughs that highlight key agreements and supplier engagements.

Engage the right departments

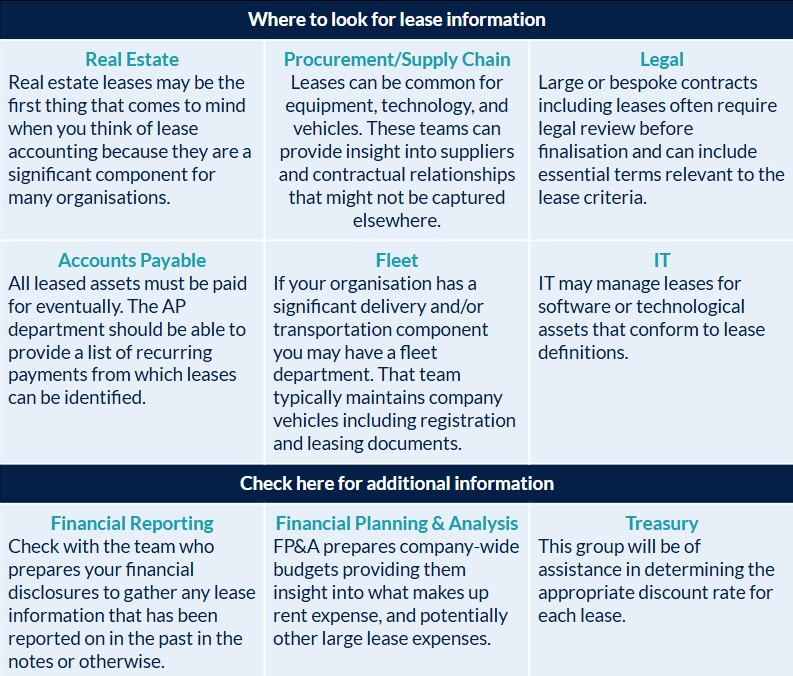

A successful lease inventory requires an interdepartmental approach. Don’t limit your search to just one department. Here are some key teams to connect with:

Establish a communication strategy early, ensuring that each department understands the importance of the inventory for ensuring compliance with FRS 102 updates.

3. Consolidate your leases in one place

Create a unified template

Develop a standardised lease inventory template that can be completed by each involved department. This template should capture essential details including:

- Lease dates and terms

- Payment obligations

- Asset details

- Information regarding embedded lease elements

Cross-check for accuracy and completeness

Once you’ve collected the data:

- Reconcile with Physical Assets: Reach out to facilities or location managers to confirm the physical presence and usage of leased assets.

- Review Financial Records: Compare your lease data against recurring payment schedules from accounts payable. This step ensures that all ongoing lease obligations are captured.

- Audit Previous Disclosures: Cross-check your new inventory with prior company disclosures. This comparison can highlight any gaps or discrepancies needing attention. A meticulous cross-check will help ensure that your inventory is both comprehensive and accurate, thereby reducing potential implementation issues down the line.

Summary

The transition to the updated FRS 102 lease accounting requirements is a significant project that demands attention to detail and collaborative effort. By clearly scoping, identifying, and consolidating your lease agreements, your organization can streamline the update process and secure more reliable and compliant financial disclosures. Although the process may initially seem time-consuming, establishing a solid foundation will pay dividends in improved compliance and operational efficiency over the long term.

By following these steps, your organization will be better positioned to handle the intricacies of FRS 102 updates efficiently and effectively.