Whether you’re an accounting student or a seasoned professional, you’ve likely encountered the term “incurred”. While it most commonly refers to incurred expenses, the term carries several meanings — ranging from standard applications to more uncommon instances that we will explore throughout this blog.

Incurred expenses in accounting

The most common instance of “incurred” in accounting is when we are referring to expenses. An expense is incurred when you have received economic benefit from a good or service. This is almost always associated with accrual accounting due to the matching principle.

Let’s take a look at two examples of incurring expenses.

First, we’ll take a look at incurring an expense that is paid for in the current period. We’ll also take a look at another instance where the expense is incurred in one period but then the cash is paid in another.

Example: Incurred expense paid in current period

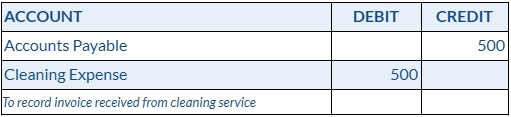

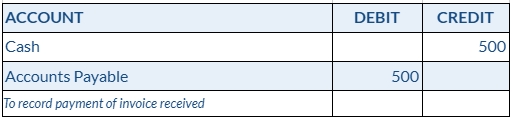

For example, suppose a company has routine cleaning services performed in their office space. The cleaners perform the service on the 5th of the month, and the company receives a $500 invoice on the 10th. At this point, the expense is incurred on the 5th because the benefit has been received and the company now knows how much the expense is due to the received invoice. When the company pays the invoice on the 12th, the expense has been officially paid within the same period it was incurred.

Journal entries: Incurred expense paid in current period

Example: Incurred expense paid in different period

Let’s now take a look at a common instance where expenses are incurred in a different period from when cash is paid.

In most cases, utility services have some sort of time lag from when the service for the utilities are provided and when the bill for the utilities is received and paid.

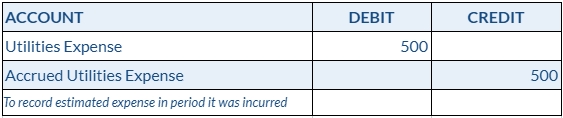

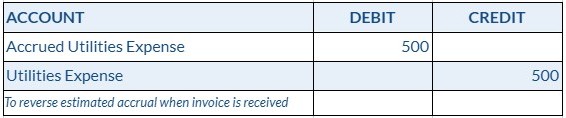

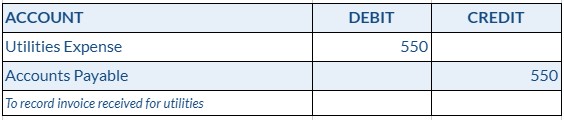

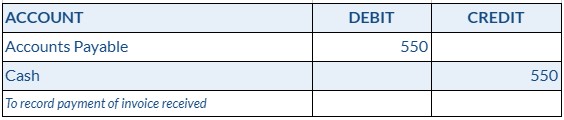

For this example, let’s say a utility bill for March was for services dated between March 1st and March 31st. The bill for March’s utilities was not received until April 10th, and the bill was paid on April 13th.

In this case, the expense was incurred in March for the amount of the bill received in April. The incurred expense is then paid for in the following period, April. This is a common example of an accrued expense for the month of March.

Since the matching principle of accrual accounting must be utilized, the expense for the utilities is recognized in the month it provided benefit, even though payment occurs in the following period. Therefore, an estimated amount of this expense must be accrued until the bill is paid. This accrual will then need to be reversed in the subsequent month once payment is made, since the accrual will no longer be necessary.

This reversal step is often done automatically when using a software solution to handle accruals.

Journal entries: Incurred expense paid in different period

Less common instances of “incurred” in accounting

Another instance of the term “incur” is when a liability is incurred. For example, if a loan agreement is executed and the funds are received same-day, a liability has been incurred even though no payments have been made. The loan payments are not obligated to be paid as of the date the funding was received. Nevertheless, that is the period in which the liability was incurred.

Additionally, costs related to fixed assets of capitalized assets can be incurred. Since costs of constructing a new asset are often capitalized, they are incurred throughout the construction process which will then ultimately be capitalized. These incurred costs will then be recognized through depreciation expense once the asset is capitalized.

Summary

The meaning of “incurred” in accounting often refers to incurring expenses. Expenses are incurred when benefit is received from a good or service regardless of when the expense is paid. To dig deeper into how to properly record expenses incurred in different periods from when they are paid, make sure to check out our blogs on accrued expenses and prepaid expenses.