What is depreciation?

Depreciation is an accounting method used to spread out the cost of an asset over its useful life, to reflect its reduction in value from wear and tear or obsolescence. Depreciation generally applies to a company’s fixed assets or to its leased right-of-use assets from finance leases.

Depreciation expense

Depreciation expense is an income statement item recognized throughout the life of the asset as a “non-cash” expense. While there are various methods of recognizing depreciation expense, discussed below, the total amount of depreciation recorded throughout the life of the asset doesn’t change, instead, the timing of the expense is what changes.

Accumulated depreciation

At the same time that depreciation expense is recorded as a debit, accumulated depreciation, a contra asset account that is the associated balance sheet line item for depreciation, is recorded as a credit. This contra asset account represents the reduction of the asset’s value over time and has a normal credit balance.

Accumulated depreciation offsets a fixed asset’s balance. As such, an asset’s net book value (NBV) at any particular point in time is its historical cost minus its accumulated depreciation balance.

Until the asset is disposed of, accumulated depreciation sits on the balance sheet, and at disposal, the accumulated depreciation is debited to clear it off the books.

Depreciation methods in accounting

Under US GAAP, there are four methods of calculating depreciation that an organization can use:

- Straight-line method of depreciation

- Declining balance depreciation method

- Sum-of-the-years’ digits depreciation method

- Units of production depreciation method

This article discusses the units of production digits method.

Units of production depreciation method

The units of production method calculates depreciation based on how much an asset is actually used, rather than simply how much time passes. Instead of expensing the same amount each year, this method ties depreciation directly to use of the asset.

Under this method, depreciation expense is determined by:

- Calculating a depreciation rate per unit of activity

- Multiplying that rate by the number of units produced during the period

Depreciation fluctuates year to year depending on production levels. If the output (units used) is high, expense is higher. If the output slows down, depreciation decreases accordingly. Unlike time based depreciation methods, this approach aligns expense recognition directly with operational activity.

Example: Units of production depreciation method

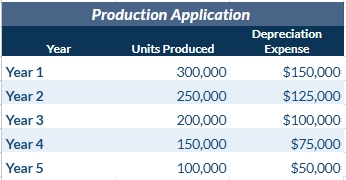

For example, assume we are a manufacturing company that purchases an industrial printing machine with the following facts:

- Purchase Cost: $550,000

- Estimated Salvage Value: $50,000

- Estimated Total Production Capacity (Total Expected Units the Asset will Produce): 1,000,000

- Depreciable Base (Purchase Cost – Estimated Salvage Value): $500,000 ($550,000-$50,000)

Step 1: Calculate the depreciation per unit

This means every unit produced will expense $0.50 of depreciation.

Step 2: Apply actual production

Each year’s depreciation is calculated as: Units Produced x 0.50

At the end of Year 1, accumulated depreciation is $150,000. The net book value (purchase cost – accumulated depreciation) is: $550,000 – $150,000 = $400,000

Depreciation continues based strictly on output until total accumulated depreciation reaches the $500,000 depreciable base. The asset will never depreciate below its $50,000 salvage value.

Journal entry example (Year 1)

Each year, the entry adjusts based on actual production which changes to depreciation expense amount.

Units of production depreciation: When does it make sense?

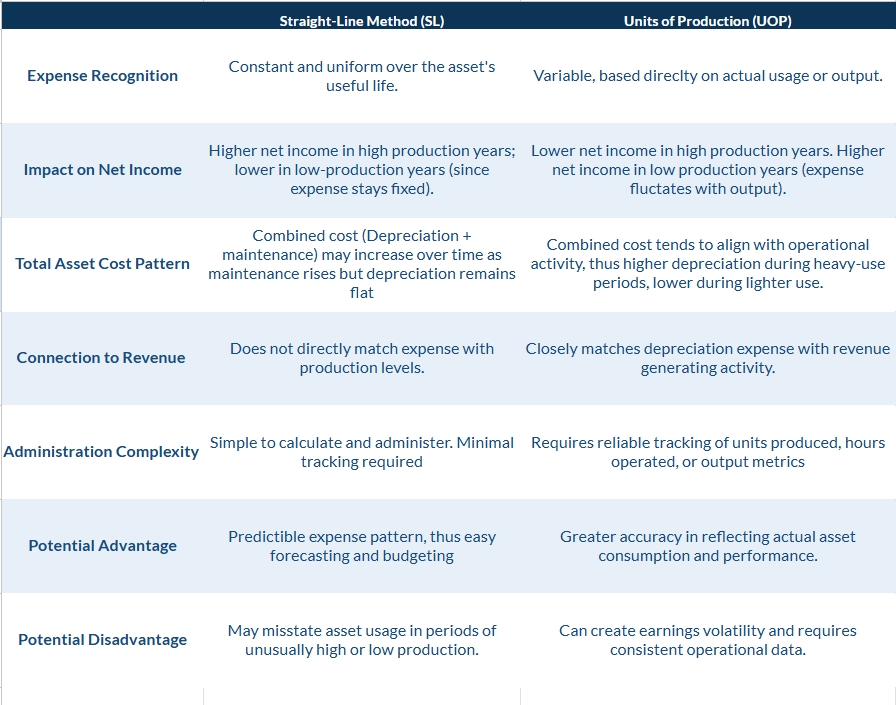

While straight-line is often the simplest and most commonly used method, the units of production method is more appropriate when an asset’s wear and tear is directly tied to usage rather than age.

This is particularly relevant when:

Variable Usage Drives Value

If the asset generates economic benefit based on output (such as units produced, hours operated, or miles driven), depreciation should follow that pattern. This improves matching of expenses with revenue.

Physical Wear is Usage Based

Some assets deteriorate primarily from operational use rather than the passage of time. In these cases, time based methods may misstate expenses in both high production and low production periods.

Production Levels Fluctuate

Companies with cyclical or seasonal outputs may prefer units of production because it mirrors operational performance. During slower periods, depreciation expense naturally declines. During peak periods, expense increases with heavier asset utilization.

Examples of common assets include:

Manufacturing Equipment

These are machines used in production environments where useful life is better measured in machine hours, cycles, or units produced rather than years. For example, a molding machine may be expected to produce 2 million units over its lifetime. Depreciating it based on actual output better aligns expense with the revenue it helps generate.

Aircraft Engines

Aircraft engines are commonly depreciated based on flight hours or cycles (takeoffs and landings). These engines may technically remain in service for many calendar years, but maintenance intervals and useful life are driven by operational use, not age alone.

Extraction Equipment

Equipment such as drills, excavators, and haul trucks often wear out based on the volume of material extracted rather than time in service. Since usage directly ties to resource depletion, units of production provide a more accurate reflection of economic consumption.

Units of production depreciation vs. straight-line depreciation

Summary

Multiple depreciation methods exist, but the units of production method is particularly useful when asset consumption is tied directly to activity levels rather than passage of time.

Although it requires more detailed tracking of output, this approach provides a more accurate representation of how the asset’s economic benefit is consumed. For industries where production volume drives asset wear, the units of production method offers a clearer tie between operational performance and financial reporting.