In this blog, we will explore salvage value and residual value, how they differ, and an example of how this comes into play when considering tangible assets.

What is salvage and residual value?

Salvage value is the estimated worth of an asset at the end of that asset’s useful life. In most cases, salvage value and residual value are interchangeable. However, there are a few minor nuances:

| Salvage Value | Residual Value |

|---|---|

| Tangible assets | Intangible assets |

| Estimated amount you receive when you sell or dispose of an asset after its useful life, often focuses on the final raw worth | Remaining value of an asset at the end of an amortization period, often assumed to be zero because the asset typically becomes obsolete or cannot be sold on its own. |

Why is salvage value important?

Salvage value is an accounting estimate that takes careful consideration. Salvage should take into account economic and industry factors to accurately estimate the value of the asset. Also, any necessary costs associated with the disposal of the asset should be factored into the salvage value that is determined.

Salvage value is a key component of determining depreciation. In this blog, we will use the most common type of depreciation which is straight-line depreciation. Straight-line depreciation is determined by taking the purchase price of an asset less its salvage value divided by the asset’s useful life. This equation will result in the depreciation expense recognized for an accounting period.

Example: Salvage and residual value

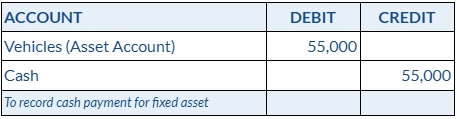

Let’s say we purchase a $55,000 vehicle. This vehicle has a four-year useful life given our industry and use for the asset. The salvage value for this particular vehicle is estimated to be $7,000 when reaching the end of its four-year useful life.

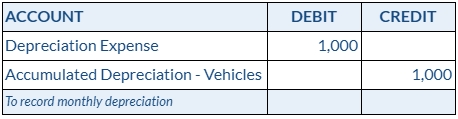

We will be using straight-line depreciation for our example. So remembering our formula of purchase price ($55,000) less salvage value ($7,000) divided by useful life (48 months), we have a monthly depreciation of $1,000 for this vehicle. $55,000 – $7,000 = $48,000 / 48 = $1,000.

For our first month we would record the purchase of the asset. The journal entry is shown below:

Each month during the 48 month period we will record an entry to record our depreciation expense and amortize the asset. The journal entry is shown below:

This will be done until we get to the end of the 48 month period which will amortize our asset to the $7,000 salvage value.

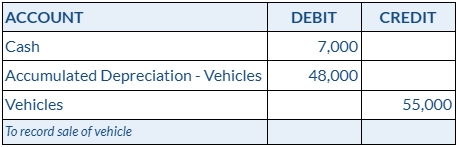

Once we have proceeded with the disposal of the vehicle for the estimated $7,000 value we will record the entry to show proceeds from the sale and remove all associated asset balances. The journal entries are shown below:

Note, there is no gain on sale since proceeds received were equivalent to our salvage value.

What if changes occur to salvage value?

If changes occur to salvage value (such as an asset being disposed of sooner therefore a higher value when being disposed), the effect is recognized prospectively. We would simply take our current book value (undepreciated value of the asset) less the new salvage value divided by our remaining useful life. This would generate our new depreciation expense that we would record until the end of the asset’s life.

Summary

Salvage value and residual value are the same concept applied to different asset types. This value is the expected amount the asset will be worth when reaching the end of its useful life for that specific organization. Careful consideration is required when determining the salvage value that way we can appropriately record depreciation.