As accountants and business professionals, it is important to master the nuances of depreciation. In this article, we will cover the double-declining balance (DDB) depreciation method, including when and where it is most utilized. We will also provide an example.

What is depreciation?

First, let’s define depreciation and why it is vital for organizations to recognize it in their assets.

- The Process: Depreciation is the process of recognizing and spreading the cost of a physical asset over its useful life.

- The Asset Balance: Essentially, we are taking the balance of an asset over the given time it is being used for business purposes.

- The Goal: The primary objective is to distribute that cost as a depreciation expense over the life of the asset, acknowledging that the benefits and service efficiency will likely diminish over time until the asset no longer provides benefit.

Why do we depreciate assets?

Businesses purchase or procure assets—generally noted as Property, Plant, and Equipment (PP&E)—intended to deliver specific services over time.

- Financial Accuracy: These appear as fixed assets on an organization’s financial statements and must be depreciated to match the purchase cost to the revenue being generated over its useful life.

- Revenue Matching: For example, if you use a truck for 10 years to help generate revenue, you need to recognize the expense incurred across those same 10 years.

- Asset Life Cycle: After that period, the asset may no longer operate effectively, at which point it is fully depreciated unless there is a salvage value—the price you expect to receive upon disposal.

Selecting a depreciation method

There are a few ways to allocate these costs, and it requires professional judgment to determine how an asset will be consumed over its life.

The most common methods include:

- Straight-Line Depreciation: The most frequent model, where the asset’s cost (minus salvage value) is charged to the income statement evenly over its life.

- Units-of-Production: Relates depreciation to the asset’s actual physical output or hours of usage rather than the passage of time.

- Accelerated Methods: These methods result in higher depreciation expenses in the early years of an asset’s life and lower expenses in later years. This category includes double-declining balance and sum-of-the-years digits.

Why select an accelerated depreciation method?

An organization might use an accelerated method if an asset is expected to generate significant revenue in the early years that diminishes over time.

A great example of this is a 3D printer:

- High Initial Volume: In the first five years, the printer might produce 200–300 units per month.

- Diminishing Returns: After five years, that capacity might drop to 150 units—half of its original output.

- Strategic Balancing: Accelerated methods help balance higher early depreciation with the higher maintenance costs that typically occur later in an asset’s life.

Example: Double-declining balance depreciation method

This approach applies a constant rate to the beginning balance of the remaining depreciable base each period.

To see this in practice, let’s look at a realistic scenario for our shop. We recently purchased a high-output 3D printer to produce specialized tools and crafts.

- The Investment: $100,000

- The Strategy: Because we are printing at high speeds to fulfill custom orders, this printer provides its maximum value and precision right now.

- The Decline: Over a 10-year useful life, its mechanical integrity will naturally diminish. It will still function, but it will eventually lose the efficiency required to meet our high customer demand.

- The Salvage Floor: After 10 years, we expect to sell the unit for $10,000 to a hobbyist or a smaller startup.

To capture this rapid early-stage utility, we use the double-declining balance method.

How the Math Works

- Determine the Straight-Line Rate: Divide 1 by the useful life (e.g., for a 10-year life, the rate is $1/10$ or 10%).

- Double the Rate: Multiply the straight-line rate by 2 (In our example, 20%).

- Apply to Carrying Value: This constant rate is applied to the remaining book value at the start of each year.

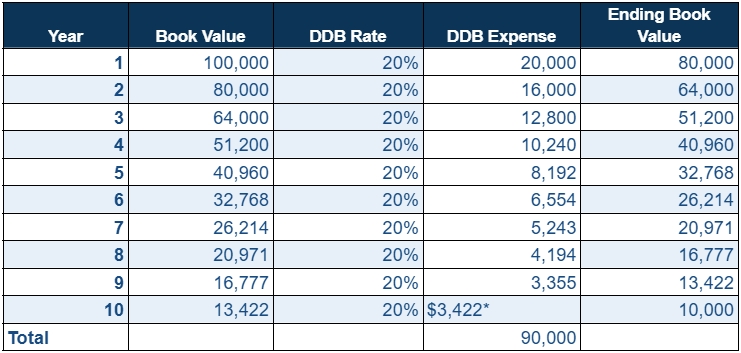

* In the last period, we take the remaining amount ($13,422) and subtract the salvage value ($10,000) to get a final expense of $3,422. This “plug” ensures the asset remains on our books at its exact expected salvage value.

The 3D printer provides the most revenue benefit in those early years. By applying the 20% rate, the schedule correctly reflects high initial depreciation that declines over the 10-year period. As you can see, the final five years show much lower amounts of depreciation. By year 10, the value depreciated down to its salvage value on the books, at which point the business would likely dispose of or sell the equipment.

Summary

The double-declining balance depreciation method is ideal for assets that provides the highest utility in its earliest years. Though requiring more oversight than the straight-line method, the double-declining balance method ensures that financial statements present a true and fair view of an entity’s position, particularly for assets that face their heaviest wear-and-tear in the initial years of operation.